Fracking has made America the center of global oil production and the engine of the world’s economy. But haste makes waste. America’s new oil wells are releasing natural gas as well, which is prized as a clean and reliable fuel around the world but must be simply burned off or “flared” if there are no pipelines to bring it to the customers that need it. The pace of the oil boom and the challenges of building new pipelines have forced oil companies to flare staggering quantities of natural gas. Texas and North Dakota are now flaring—that is, wasting—more gas than many states or even nations consume. This Article shows that to stop this economic and environmental waste, states must develop a new approach to antitrust law. It makes the case for state energy cartels.

One of the few consensus grounds for regulation is preventing abuse of market power—preventing dominant suppliers from increasing their profits by selling less at higher prices. States break up producer cartels so that competition provides consumers with lower prices. But what happens when a state’s interest coincides with producers rather than consumers? The economic health of major energy exporters depends on the price of the products they export. That is, these states, provinces, and countries can benefit by increasing the price of the oil and gas. For the first half of the twentieth century, the United States was the world’s premier oil exporter; during that time, U.S. states cooperated as a de facto cartel to ensure higher oil prices. When other countries overtook the United States as the world’s top oil producers, they formed the Organization of Petroleum Exporting Countries (OPEC) to play a similar role.

This Article explains how state cartels offer the best solution to the flaring crisis and a unique opportunity for productive global cooperation to address climate change. It shows how states can slow production, protect the environment, and increase their industries’ profits by adapting and perfecting tools that the United States stumbled upon in the first half-century of oil production. And it shows how these tools can be tailored to protect consumers, industry, and the environment.

Introduction

It is difficult to exaggerate the power of OPEC, the Organization of Petroleum Exporting Countries, which coordinates production of oil by many of the world’s leading exporters. The world’s economies tremble in anticipation of its every communique. When OPEC restricts production, world oil prices rise; and when oil prices rise, the global economy suffers. Since World War II, all but one U.S. recession was preceded by rising oil prices.1

Why would these oil-producing countries conspire to cut oil production? The answer is that OPEC is the world’s most prominent example of market power—the monopolist’s ability to raise profits by cutting production.2 In past decades, these countries together controlled a large enough share of world production that when they cut their production, prices rose enough to more than compensate them for selling less oil.3 That is, what these countries lost in lower sales volume, they more than made up for in higher sales prices.

But these oil behemoths are also different from a normal monopolist in two ways. First, they are sovereign nations so they must balance the interests of oil consumers in their country with their oil producers’ interest in high prices. Second, they are managing a long-term resource: their vast stores of oil wealth. They have to consider the long-term value of this resource, ensuring that prices are high enough that they do not run out of oil and simultaneously making sure prices are low enough that alternatives such as ethanol and electric vehicles do not become too attractive.

How rapidly should these countries produce oil? To answer this delicate and fateful question, the OPEC cartel can rely on the field of conservation economics, developed in the United States in the first half of the twentieth century to manage its own oil wealth, which at the time dominated world supplies.4 The short answer is that a country with dominant market power should produce oil rapidly enough that the price of oil is affordable but gradually and smoothly rises over time as supplies dwindle.5

The United States, unexpectedly, is facing this momentous question again because it is emerging from history’s biggest oil boom, driven by directional drilling and hydraulic fracturing.6 This combination of technologies, generally known as “fracking,” has more than doubled American oil production in just a few years and turned the United States into one of the world’s leading oil and gas exporters.7

As an energy exporter, the United States will have to face the central issue that has driven OPEC—what rate of production would maximize the value of its vast, newfound oil and gas reserves? In fact, it may find itself increasingly aligned with the oil-exporting countries in OPEC, with the same interest in smoothing global production of crude oil.8 That dynamic is already developing as the United States increasingly works with Saudi Arabia to ensure that U.S. sanctions on Iran do not disrupt global oil supplies.9 And it has accelerated as the March 2020 collapse in global oil prices sparked U.S.-OPEC negotiations on oil prices and production.10

As momentous as these oil questions are, there is an even more pressing governance crisis: over-production of natural gas. Fracked oil wells also produce “associated gas”—natural gas molecules that are trapped together with the oil now being produced from shale rock layers.11 These gas molecules are released along with oil when shale rock is threaded by drilling horizontally and then hydraulically fractured.12 When this gas reaches the top of the wellhead, the oil company can separate it from the crude oil and ship it by pipeline to natural gas consumers.13 But if there is not yet a pipeline to bring this natural gas to markets, or if local markets are already over-supplied with gas, an oil company considering drilling a new well faces a difficult choice. In theory, it could wait to drill for oil until a pipeline is built for gas, but oil companies typically need immediate oil production to pay the rotating debt that finances their investments.14 Or it could drill the well, sell the oil, and simply burn or “flare” off the gas.15 Oil companies in Texas’s Permian Basin and North Dakota’s Bakken Shale are increasingly drilling immediately, profiting from shale oil and flaring off more and more associated gas.16 By 2019, oil wells in each of these formations were flaring more gas than many states consume; together these two formations are flaring more gas than is consumed by all 49 million people in Colombia.17

This tremendous economic and environmental waste is just a more severe and localized version of the age-old oil exporter dilemma: a race for production often fails to maximize the long-term value of the hydrocarbon resource. Oil companies cannot solve this dilemma by themselves. If a single oil and gas producer slowed its drilling, it would do nothing to raise gas prices; it would only delay its profit from oil production. But if oil companies tried to band together and slow production so all companies could benefit from higher natural gas prices, they would be criminally liable for price-fixing under the Sherman Act.18

By contrast, states and nations have tools for maximizing the long-term value of their oil and gas resources. These tools were developed in the United States in the first half-century of the oil industry when American oil ruled the world.19 These tools fell into disuse in the past half-century as the United States became a net-energy importer, identifying its interests with consumers in need of cheap energy and not with producers looking to prop up the value of their goods.20 Now, as history’s biggest commodity boom returns America to its place as a leading global energy exporter, the United States must adapt these old tools to ensure maximum benefit from the new boom.21

This Article shows how the nation and its fifty states can maximize the long-term benefit from the unprecedented oil and gas boom by minimizing environmental and economic waste. It examines antitrust law from a novel angle, showing what happens when the state’s interest is aligned with producers rather than consumers.22 It develops the theory of state cartels, showing how jurisdictions can maximize the long-term value of their natural resources by slowing production and banding together with other producing jurisdictions. And it shows how this novel theory both increases the economic value and decreases the environmental cost of energy production and could be employed to address the nation’s crisis of natural gas flaring.

This Article also shows why state cartels create a unique opportunity to harness the self-interest of the world’s oil and gas superpowers to slow global climate change. State cartels increase the profits of oil and gas producers, but they also dramatically slow production and use of fossil fuels. If the United States can use its new dominance of global energy to coordinate production cuts that raise global oil and gas prices, it will increase cash flow to Saudi Arabian, Russian, and American oil companies, while making concrete progress on climate change and encouraging cleaner technology.

Even if U.S. states only cut back production enough to stop flaring, they can still win huge environmental benefits. Natural gas burns much more cleanly than dirtier fuels, such as oil and coal, that provide heating and power to much of the world.23 When natural gas is flared at the well, it is just an environmental liability. If natural gas can be saved and transported to the markets that need it to replace oil and coal, it will be an environmental asset, providing cleaner air around the globe.

The argument unfolds as follows. Part I explains the economic theory of state energy cartels—showing why exporting states can profit more by producing less energy and explaining how they can optimize the pace of production. Part II unearths the history of state oil cartels, showing how, at first, states such as Texas, and then later, OPEC and Saudi Arabia, worked to moderate the pace of oil extraction. Part III explains how the Texas Railroad Commission and the Interstate Oil and Gas Compact Commission, a product of the first U.S. oil boom, can resume their crucial role and work to limit natural gas flaring, increasing the economic benefit from America’s huge oil and gas bounty. Part III also explains how its proposal secures significant environmental benefits, provides a unique opportunity for global cooperation on climate change, and prepares the United States for its future as an oil exporter.

I. The Theory of State Cartels

Breaking up monopolistic cartels is one of the fundamental justifications for the modern regulatory state.24 A cartel that can coordinate to lower production will do so to raise prices above the marginal cost of production, so that it can make more money even as it sells less.25 This output restriction means consumers must pay more money to producers and reduces the economy’s efficiency by pricing out customers who would be happy to buy goods at their cost of production.26 But in the unusual case when a state produces much more than it consumes, exporting commodities for consumers elsewhere, the state’s interests tend to align with producers. Its citizens get swept up in the supply chain of commodity production as landowners, manufacturers, investors, laborers, and service workers, so that they benefit more from high prices than they lose from low prices. As a result, the state may gain more from higher prices that make its producers more profitable than it loses by harming its consumers or reducing the efficiency of the economy.27

In this counterintuitive situation, the state can function somewhat like a cartel, coordinating and constraining production of independent producers to maximize their long-term profits. Such a cartel only works when the state is a dominant producer in the commodity market or can form an alliance with other major producing states. But dominant producers are common within natural gas commodity markets because transport constraints divide global markets into many smaller markets, many of which are served by a dominant gas-producing state. These gas markets are ripe for a rise of new state energy cartels.28

A. The Case for State Cartels

Monopolies have costs for consumers and the economy, but they benefit producers. If a state is dominated by producers, a monopoly’s benefits may sometimes outweigh its costs. In these counterintuitive circumstances, the maxims of antitrust and competition law are turned on their head. To know when the state should allow, encourage, or even enforce a cartel, it must measure and compare the costs and benefits of monopoly.

1. The Costs and Benefits of Monopoly

In a competitive marketplace companies aim to sell as many items as they can produce at a profit because their profits fall when they sell less. “Market power,” by contrast, is the ability of a dominant player, or group of players, to raise its profits by cutting production—the monopolist controls so much of the market that when it cuts production and prices rise, it gains more from higher prices than it loses from fewer sales.29 This price rise harms consumers, as can be seen in the standard supply-and-demand charts contrasting efficient markets with a monopoly.

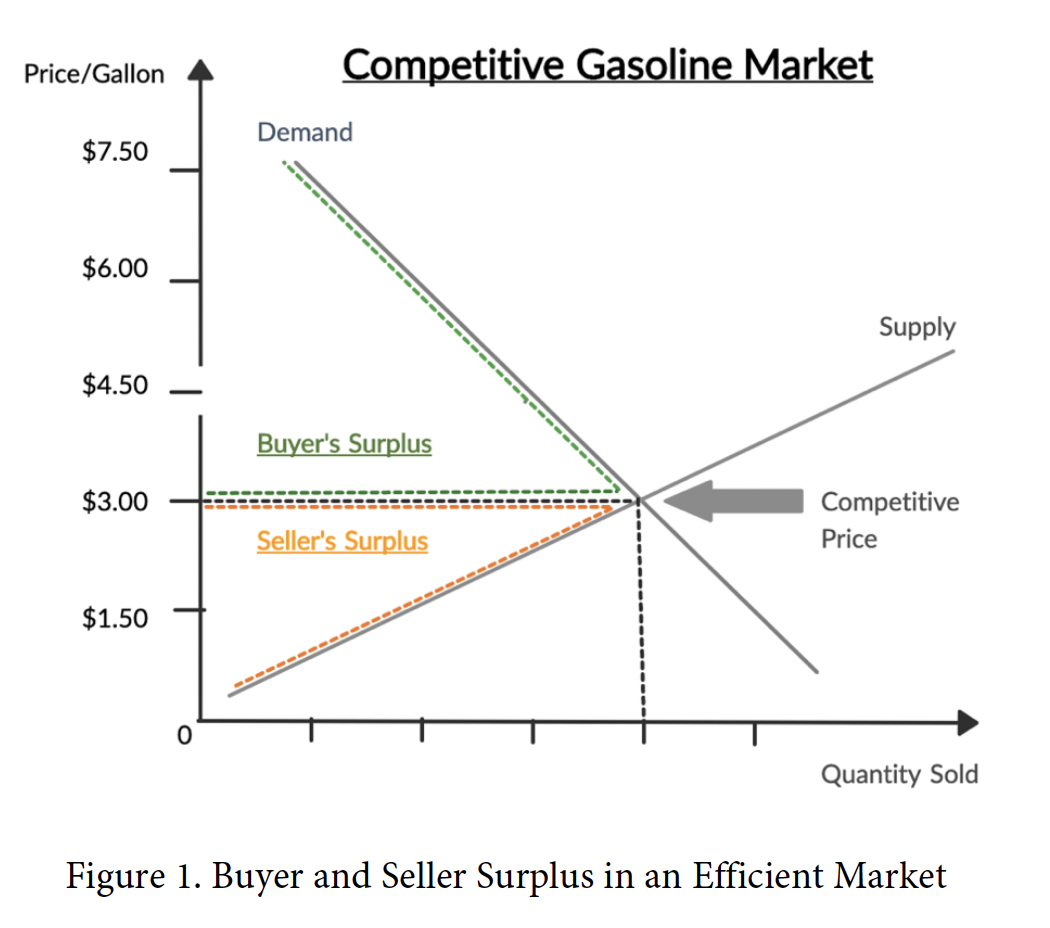

Take the market for gasoline. Imagine an efficient market with an equilibrium price of $3 a gallon. Low-cost producers and eager buyers split the large surplus in the market. If a producer can make a gallon of gasoline for $1 per gallon, it will make a profit of $2 per gallon. A more marginal producer who can make a gallon of gasoline for $2.50 makes $0.50 per gallon. The area between the supply curve and the equilibrium price on the supply-and-demand chart shows this producer surplus.30 (See Figure 1.) Buyers get a big surplus from the market too: if a consumer would have been willing to pay up to $7 per gallon, she receives a surplus of $4 per gallon when she is able to purchase it for just $3 per gallon. A more price sensitive consumer that would only have been willing to pay $4 for a gallon gets a surplus of $1 per gallon. The area between the demand curve and the equilibrium price shows this consumer surplus.31

When a single seller takes over a market, however, it can win more than the usual seller surplus by reducing production. So, imagine that a single seller corners the gasoline market and cuts supply 25%. (See Figure 2.) As buyers scramble to secure gasoline in this artificial shortage, the equilibrium price rises sharply—imagine a rise from $3 a gallon to $4.50 a gallon.

The monopolist receives higher prices for its product and lowers its costs by shutting down its highest-cost production facilities. True, it foregoes some marginal sales by restricting supply. If it kept operating all the facilities that operated in the efficient market, it could turn a small profit on running facilities that cost $2.50 a gallon to produce gasoline for that $3 a gallon market. But the monopolist gains more from higher prices and lower costs than it loses from forgoing a few marginal sales. In other words, the area between its supply curve and the market price has increased.32 (See Figure 2.) Accordingly, the buyer surplus is reduced by higher prices—the area between the demand curve and the market price has decreased.

Absent distributional concerns, the main cost of monopoly is the reduction in sales that results from the monopolist restricting supply to marginal consumers. Although we often think of excess profits taken from consumers as the problem of monopoly, the extra money that consumers pay for gasoline goes to the monopolist, so at least someone benefits.33 But the foregone gasoline sales are simply a deadweight loss—no one benefits. If a seller could have produced a gallon of gasoline for $2.50 and sold it for $3 to a consumer that would have been willing to pay $4, then the seller would have been better off by $0.50 and the buyer would have been better off by $1. When a monopolist restricts supply to raise prices, this trade can no longer happen, and society is poorer.34

Apart from this deadweight loss from foregone sales, most politically responsive governments also share the consumer’s distributional preference for lower prices to ensure a large buyer surplus. That is, the government usually favors lower prices to ensure that consumers receive a reasonable share of the market surplus. So, in practice, monopoly regulation often focuses on lowering prices as well as increasing supply.35 Governments generally try to limit market power by breaking up monopolies or prescribing the prices that monopolists can charge.36

2. When Cartels Serve the State Interest

Sometimes, however, the government is the monopolist. Almost everywhere other than the United States, oil, gas, and other minerals under private landowners’ land are owned by the government, so higher prices for oil and gas would maximize government revenue.37 Of course, the government may benefit politically from lower prices for consumers.38 But if the government produces oil and gas for export to consumers in other countries, it will prefer higher prices to extract more revenue from those foreign consumers.39

Even in jurisdictions like the United States, where private landowners own most oil and gas and it is produced by private companies,40 governments may enforce a cartel to raise oil and gas prices.41 That is, individual states can and do control the overall rate of oil production, so they can make all companies slow their oil production simultaneously.42 If a state’s companies, in aggregate, enjoy market power, the state may raise their profits by forcing all companies to cut back production to ensure higher prices.

If oil companies agreed among themselves to cut back production, they would violate the Sherman Act, but industry compliance with state limits on production does not.43 The state may not simply authorize companies to cooperate in raising prices as much as they like.44 But the state may set its own production limits or even authorize industry-set limits so long as these limits are “clearly articulated and affirmatively expressed as state policy” and are “actively supervised.”45

When would a state want to take advantage of its ability to enforce a cartel to raise prices? Roughly, a state would want slower production when its producers have more to gain from high oil prices than its consumers and its economy have to lose. So, raising prices helps a state when its producers gain so much from their increased surplus that it more than makes up for the diminished surplus of its consumers.46

Thus, even when the government does not own a country’s oil, if the country is an oil exporter, it may want to maximize the value of the nation’s oil when it believes its landowners and oil companies have more to gain from high oil prices than its consumers have to lose. More precisely, a government that seeks to maximize utility for its own citizens will favor a cartel when gains to its producers outweigh the costs to its consumers. In these circumstances, the valence of antitrust and competition law is flipped on its head and a utility-maximizing government may tolerate, sponsor, or even enforce a cartel or other form of supply restriction.47

B. How States Optimize Oil and Gas Production Rate

When a state has an interest in sponsoring or enforcing an energy cartel, it faces a second question: How much should it restrict supply? This is a question that monopolies face every day. A monopoly will restrict supply to maximize its producer surplus, regardless of the impact on consumer surplus, or the increase in deadweight loss, but mindful of the danger that huge profits could induce other producers to compete with it.48 As a result, it will restrict supply, selling less at higher prices, until further restriction would cost it more money from lower sales than it would gain from higher prices.49 That is, it will cut supply until the marginal revenue that it would lose from cutting another unit is equal to its marginal cost of production.50

For states managing oil and gas cartels, the question is more complicated in two respects. First, the state must also consider its consumers, so it will take reduced consumer surplus and deadweight loss into account to the extent that they fall on consumers within the state. Second, the state is managing a long-term, finite oil and gas resource, so it must also consider how changing the rate of production will change the value of this resource over time.

First, how should a net commodity-exporting nation balance the interests of producers, consumers, and the economy? Like a monopoly, it knows that restricting supply until marginal revenue equals marginal cost would maximize its producers’ surplus. But the state will also consider consumer surplus to the extent that those consumers are citizens, which means that it will not want to restrict supply as much as a monopoly would. To maximize domestic surplus, it will want to maximize its producers’ surplus plus its consumers’ surplus, restricting supply somewhat but less than a monopoly would.

Another approach is to expressly distinguish domestic consumers from foreign consumers, restricting exports only. This is the approach taken by many oil producers in the developing world: making oil available to domestic and foreign markets at different prices.51 In this situation, the government could, in theory, restrict exports to the same extent that its exporting industry would choose, maximizing producer surplus from these exports. But all price discrimination is imperfect—there is some leakage between sets of consumers paying different prices.52 For one thing, if foreign markets are paying higher prices, domestic consumers will be tempted to illegally export fuel to benefit from those higher prices.53

Second, how fast should a major oil and gas exporter extract and export its finite resources? This question was urgent in the United States in the years between the world wars, when it produced two-thirds of the world’s oil.54 An associate professor of mathematics at Stanford University, Harold Hotelling, produced the answer in 1931: a monopolist should produce more at first and less over time.55 To understand this result, imagine that you held all the oil in the world in a warehouse and could sell it whenever you wanted to: selling more oil at first and less over time ensures that the price of oil rises smoothly over time, in parallel with the overall growth rate of the economy.56 This means low prices at first, which ensures that consumers find uses for oil and also discourages consumers from finding alternative sources of energy.57

Hotelling showed that this price path strategy was optimal because if oil prices rose slower than the overall economy, then a producer could profit by simply selling more oil immediately and investing in the wider economy.58 On the other hand, if oil prices were set to rise more rapidly than the economy, then the producer could benefit by withholding some oil and selling it later at higher prices.59 Thus, a rational oil monopolist would ensure smoothly rising prices over time.60 This is the logic that has driven the dominant oil powers over the past century of oil production.

C. When State Oil and Gas Cartels Work

Recall that a large producer can only increase its profits by restricting supply when it has “market power”—when it controls so much of the market that producing less increases prices enough to outweigh the cost of fewer sales. No single state can exercise market power in the world’s oil market that connects our global oceans’ countless ports of call, because no country produces more than an eighth of the world’s oil.61 If Russia unilaterally cut its oil companies’ production by twenty percent, other countries would take advantage of these higher prices by shipping more oil. The final result would be slightly higher world oil prices but not enough to compensate Russian companies for producing twenty percent less oil.

Oil and gas market power can still emerge in two ways. First, enough producing states can band together to restrict supply, creating an international cartel that can benefit all members by raising prices. As explained in Part II of this Article, that is the path taken by OPEC over the last half century; and OPEC is modeled on the United States’ Interstate Oil and Gas Compact Commission, which played the same role in the middle of the twentieth century.62 When OPEC’s share diminished in recent years, it formed a temporary alliance with Russia to cooperate in raising world oil prices.63 With the early 2020 fall in global oil prices, there is now talk of coordinating production cuts between the United States, OPEC, and Russia, which together dominate global oil production.64

Second, transport constraints can isolate individual markets so that local producers have market power within these local markets. This is uncommon in oil markets because oil can be transported in so many ways: by rail, truck, or ship.65 If prices are higher in one port, producers in other ports will take advantage by shipping more oil until prices roughly equalize.66 And shipping oil by tanker is cheap, so the price of oil in port markets around the world generally stays in a range of, at most, a few dollars.67 But at times there are still significant geographical differentials in oil prices, especially in landlocked markets when pipeline capacity is constrained so that oil producers that cannot find space on a pipeline must pay substantially higher prices to ship their product by rail or truck.68 In these circumstances, one jurisdiction’s oil producers can, if they act in concert, exercise market power.69

Significant geographic differentials are far more commonplace in natural gas markets because gas is always expensive to transport—it can only be moved by pipeline or as liquefied natural gas.70 Both of these options require multibillion dollar facilities and years of regulatory approvals, so marginal production may not be able to reach neighboring markets for years.71 Even if two markets are connected by a relatively inexpensive pipeline, they may act as separate markets for long periods of time if the pipeline reaches capacity before a new pipeline can be built.72 And even if there is adequate transport between two natural gas markets, the high cost of shipping gas means that distant markets always operate somewhat independently.73 As a result, if they are allowed or compelled to act together, it is extremely common for one jurisdiction’s natural gas producers to have market power within their local natural gas market.74

II. State Energy Cartels, Here and Abroad

Although the theory of state cartels has, until now, remained inchoate, states have, in practice, been enforcing and coordinating de facto cartels since the beginning of the modern oil industry.75 OPEC is the most famous example; its decisions have shaped the world economy for the past half century.76 But the first state cartel was created by the Railroad Commission of Texas in the 1930s, which then expanded to coordinate with other states through the Interstate Oil Compact Commission.77 Most recently, with even faster-shifting energy markets, the Canadian province of Alberta has adopted short-term cartel restrictions to make use of a case of temporary market power in its landlocked oil markets.78 This new approach, combined with this Article’s theory of state cartels, could allow innovative jurisdictions to flexibly use short-term restrictions to maximize the economic and environmental benefits of their energy production.

A. The Railroad Commission and the Oil Compact

The modern era began on January 10, 1901, when the Spindletop well in Beaumont, Texas, blew out and doubled global oil production overnight.79 As Spindletop’s historical marker puts it: “On this spot, on the tenth day of the twentieth century, a new era of civilization began.”80 At the dawn of the century, this gusher would fuel the automobiles, trucking, railroad engines, electrification, and shipping that would build the world we now share.81

The problem of oil overproduction, however, first came to the fore after the discovery of the East Texas oil field on October 5, 1930.82 By the next summer, this single massive oil field was producing almost a million barrels of oil per day—ten times as much as Spindletop and forty-two percent of all U.S. production.83 At the same time, the ongoing Great Depression was reducing demand for oil, so as Texas production ramped up, the price of oil dropped further and further—prices fell from $0.99 per barrel in October 1930 to $0.13 per barrel in July 1931.84 By the end of the year a barrel—forty-two gallons of oil85—cost less than a dime.86 Some barrels sold for as little as two cents.87 This was a massive waste of Texas’s oil and the Railroad Commission of Texas began a years-long struggle to conserve its long-term value.88

The Railroad Commission of Texas is economic history’s most important, and most poorly named, regulator. In 1917, the Railroad Commission was given authority over pipelines because, like railroads, they transport oil.89 In 1919, then, it seemed natural to give the Commission authority to regulate oil production as well.90 In the years that followed, it assumed a never-to-be-repeated control over the world’s economies. In 1931, the first full year of production from the East Texas oil field, Texas production jumped to twenty-four percent of world production.91 Texas maintained this dominant role for decades, producing a quarter of the world’s oil from 1931 to 1953.92 Nowadays, the world’s most dominant oil nations only produce about twelve percent of world supply.93 No nation has ever approached the global dominance that the State of Texas enjoyed during these crucial years when the world’s economy, and then the future of democracy itself, hinged on Texas’s oil wells.94

As East Texas oil field production ramped up in early 1931, the Railroad Commission stepped in, trying to slow production to raise prices for the benefit of all producers. The Railroad Commission imposed limits on daily production in April 1931.95 These limits on how much daily production is allowed, known as “allowable limits” or simply “allowables,” serve two purposes.96 First, allowable limits maximize the amount of oil that can ultimately be produced from the underground reservoir, which would be damaged by too-rapid pumping.97 Second, allowable limits can raise prices for all producers if they are imposed by a regulator that controls production from enough producers to form a cartel with market power.98

A federal court quickly struck down the Commission’s new allowables, holding that state law did not allow the Commission to set limits to raise prices.99 The court believed the Commission could set limits to protect the oil reservoir itself from damage by a race to production, but it rejected the notion of allowables to raise prices.100 The Texas legislature added to the confusion by passing a law against waste but simultaneously codifying the court’s holding against limits to raise prices.101

In the meantime, Oklahoma, with much less production at stake and correspondingly less market power, decided it could not wait for Texas to act; its Governor, Alfalfa Bill Murray, sent troops to close two of the state’s most productive oil fields until prices recovered to a dollar per barrel.102 Thirty-seven East Texas oil companies sent a telegram praising Governor Murray’s “leadership and courage” and contrasted it with the situation in Texas, where the Chamber of Commerce was begging the Governor to impose martial law to limit production.103 Of course, the companies could not simply agree to cut production themselves—that would be illegal price fixing—so they waited for Texas’s Governor Sterling to act.104

By August 16, Governor Sterling had seen enough; he declared martial law and sent in the national guard and the Texas Rangers to stop production and enforce whatever new limits the Railroad Commission would set.105 As this action raised prices, more and more Texans moved to drill wells to take advantage of the price rebound and make sure they won their share of oil before their neighbors’ wells drained it from the common reservoir.106 As a result, the Railroad Commission was forced to keep cutting the daily allowable further and further.107 Its first allowable level, in April, was 1,000 barrels per day, but that was struck down by the courts.108 Now, ignoring the court, with the Governor on its side and boots on the ground, the Railroad Commission was enforcing much stricter limits: when the troops let wells reopen, they were limited to 225 barrels per day.109 Within a week, the Commission cut allowables to 165 barrels per day.110 As more wells came online in just three weeks, the Commission cut them further to 145 barrels to keep the East Texas oil field’s overall production at 1,000,000 barrels per day, less than half of what the field had produced before Governor Sterling sent in the troops.111

Of course, as the Railroad Commission optimized production limits, and oil prices rose, there was even more reward for producing more oil in violation of those limits. Despite the best efforts of the national guard and the Rangers, this “hot oil”—oil produced beyond the allowable limits—remained a huge problem.112 Then, on February 18, 1932, a federal court struck down Governor Sterling’s imposition of martial law and the limits he had imposed on oil production.113 The Governor responded by appealing to the Supreme Court, claiming the limits were being imposed by the Commission, not the troops, and leaving most of the troops in place as roving “peace officers.”114 The Railroad Commission, for its part, responded by dropping allowables to seventy-five barrels per day.115

The year 1932 proved to be a time of regulatory defiance as the Commission issued nineteen new allowable orders, and the courts struck each one down.116 Finally, in November, the legislature passed a law explicitly allowing the Commission to cut production to raise prices.117 When the Supreme Court finally upheld the ruling against martial law in December,118 more of the troops left, but a few stayed to support the new Railroad Commission mandates, which were getting even more organized support from local industry.119 Finally, in February of 1934, the courts approved the Railroad Commission’s new authority, and its ability to enforce limits was secure.120

As Texas began to control its oil production, which accounted for forty percent of U.S. production, the federal government began encouraging other states to cooperate. First, relying on his authority under the newly-passed National Industrial Recovery Act,121 President Franklin D. Roosevelt issued an executive order banning interstate transportation of hot oil—that is, oil produced in violation of state allowable limits.122 The National Industrial Recovery Act was struck down by the Supreme Court in 1935,123 but just a month later the U.S. Congress passed a parallel law banning hot oil, the Connally Oil Act, almost universally known as the Connally Hot Oil Act.124 By the same Act, Congress authorized the states to coordinate their restrictions through a new interstate compact: the Interstate Oil Compact Commission.125

The Compact Commission proved to be one of economic history’s most important regulatory innovations. It allowed the independent states to coordinate production cuts to ensure they received maximum value for their oil and gas.126 During its prime, from 1935 to 1953, the United States produced sixty percent of world oil, at times as much as seventy percent,127 powering the recovery from the Great Depression, the Allies’ victory in World War II, and the post-war economic boom.128 Working with federal experts from the Bureau of Mines, the compact states agreed on production levels for each state.129 The individual states then set production levels for each well in the state by taking that overall level of production and then allocating it among oil fields and then, in turn, individual wells.130 Texas was the dominant player in the Compact Commission because it produced forty-one percent of U.S. oil during this period.131

When the center of oil production shifted to the Middle East in the 1960s, its new energy powers realized that they too must coordinate to maximize their oil riches.132 Naturally they turned to the model of the Interstate Oil Compact Commission.133 The organization they formed, OPEC, would dominate the global economy for the next half century.

B. The Organization of Petroleum Exporting Countries

The Organization of Petroleum Exporting Countries (OPEC) was formed in 1960, just as oil production from the Middle East was beginning to rapidly surpass the established sources in the United States.134 The year 1953 was the first in the twentieth century in which the United States produced less than half of the world’s oil.135 By 1965, the Middle Eastern countries together produced more oil than the United States.136 By 1973, the year of the great “Arab oil embargo,”137 the United States produced less than a sixth of the world’s oil, dwarfed by OPEC, which produced forty-six percent.138 Since then, OPEC’s decisions have been the single biggest factor in determining the world oil prices that shape the global economy.139

In the 1973 oil crisis the Middle Eastern OPEC countries cut overall production, embargoed exports to nations that they perceived as supporting Israel in the Yom Kippur War, and dramatically demonstrated the power of OPEC’s oil dominance.140 In the years leading up to 1973, Texas and the other American oil-producing states had given up on using allowables to ensure higher prices—they no longer had market power in a market dominated by OPEC.141 States still set allowables, but they were simply set at a level to protect common oil and gas reservoirs and thus ensure maximum ultimate recovery.142 They were not ratcheted down further to raise prices.143 And of course, higher prices would no longer have served the national interest, because in the late 1940s the United States had become a net oil importer for the first time in modern history.144 As a result, by 1973, when oil prices rose, the American states had no “spare capacity” to respond—that is, they could not ramp up production any further without damaging their oil reservoirs, which would lower their ultimate recovery of oil.145 Without spare capacity, America was helpless to watch the oil crisis unfold.

When the Middle Eastern oil powers cut their production by less than a quarter, oil prices jumped sevenfold.146 It was a complete triumph for OPEC, which found it had the same dizzying power the Railroad Commission had once exercised: it could cut its production, lowering its costs and extending the life of its oil reservoirs, while increasing its cash flow by making the world pay higher prices.147 And it ushered in decades of OPEC-managed oil prices, in which higher energy prices stunted global growth, leaving the world to plead for more production.148

Since 1973, OPEC’s decisions on production have shaped global oil markets. For example, when global oil discoveries swamped the markets in the 1980s, OPEC cut its production to ensure that oil prices did not crash.149 Again, when oil prices plummeted following the 2008 global financial crisis, OPEC cut its production, doubling world oil prices.150

Of course, the rest of the world, dependent on oil imports, has tried to resist OPEC’s market power, banding together and working to reduce their energy consumption.151 Yet none of these efforts have changed the fundamental reality that oil prices continue to shape the economy, which uses more oil every year.152 Finally, in the new century, the United States found the key to breaking OPEC’s dominance: its own flood of crude oil.153 The fracking boom is the biggest oil boom that the world has ever seen, and it may either break OPEC or forge a new alliance between the United States and the world’s other energy powers.154

The American boom dramatically decreased OPEC’s market share, limiting its market power.155 OPEC’s share of world oil production, which had at times been nearly half, fell to thirty-four percent by 2012 and thirty percent by 2019.156 As OPEC’s market share fell, its production cuts had less and less influence on global prices, and it captured a smaller share of any price increase, decreasing its incentives to restrict production.157 OPEC found a temporary solution to this problem by working with Russia to form an alliance known as OPEC+, which cooperated from January 1, 2017 until Russia abruptly withdrew on March 6, 2020.158 With the breakup of OPEC+, we are entering a new period of uncertainty for global oil supply, but one that presents a unique opportunity for the United States and the global environment to benefit from new three-way negotiations with Russia, Saudi Arabia, and OPEC.159

C. Nascent North American Cartels

North America is emerging from the biggest oil and gas boom the world has ever seen. In fact, it is emerging from three simultaneous booms that have raised North America to a completely unprecedented level of oil and gas production.160 Most important has been the boom in oil production enabled by directional drilling and hydraulic fracturing—generally known as “fracking.”161 Second, fracking has also unlocked vast reserves of natural gas production that are set to soon make the United States the world’s number one exporter of liquefied natural gas—gas that is cooled until it is liquid and shipped to gas-hungry nations in Europe and Asia.162 Third, Canadian oil production is still rising as it produces more and more from its oil sands, extracting heavy oil from sandy soils using steam or hot water.163

These booms have, at times, overwhelmed the ability of the transportation system, as companies cannot build pipelines or ramp up crude-by-rail fast enough to bring this flood of oil and gas to market.164 There is so little room in gas pipelines that producers in Texas, North Dakota, and Canada often must simply flare their natural gas or pay others to take it away.165 And even oil can trade at a substantial discount in regions where there are not yet enough pipelines to bring all the new oil to market.166 Low prices in these transport–constrained local markets have created growing economic pressure to adopt regulations to slow oil and gas production until the pipeline system can catch up. And these transport constraints have created temporary situations of market power that nimble regulators can use to protect cash flow for producers unable to get their products to market.

The clearest example is the province of Alberta. In recent years, it has faced catastrophically low local oil prices because there are too few pipelines connecting it with global oil markets.167 Even a small surplus of oil over transport capacity means that oil producers must bid lower and lower prices to secure a spot on the province’s export pipelines.168 Making matters worse, Canadian oil is so heavy and viscous that it needs to be diluted with lighter hydrocarbons to make it fluid enough to be transported by pipeline.169 In late 2018, the cost of this diluent plus pipeline transport was more than the value of a barrel of exported Canadian oil—that is, rather than receiving money, Canadian producers were having to pay people to take their oil away.170 In response, Alberta ordered all oil companies to cut their production back 8.7%.171 This curtailment was supported by many oil companies, and it immediately raised oil prices, increasing their cash flow and profits.172

Alberta’s example illustrates the surprisingly wide range of situations where regulators can exercise market power. Alberta does not have a monopoly in global oil markets; it produces under four percent of the world’s oil.173 But transport constraints mean that there is not a single global oil market: Alberta does not have enough pipelines connecting it to global markets so it is, to an extent, an isolated market.174 Alberta’s government controls production from a group of oil companies that can exercise market power within their isolated market if they work together. That is, Alberta can increase its producers’ profits by cutting their production, as its 2019 curtailment proved. When Alberta cut production by just 8.7%, heavy oil prices in Alberta tripled; enforcing a cartel to cut all companies’ production drastically increased those companies’ cash flow.175

Alberta’s isolation is somewhat unusual in oil markets because oil can easily be transported by rail, truck, or ship. But it is commonplace in natural gas markets because natural gas can only be moved by pipeline or as liquefied natural gas.176 As a result there are many, many jurisdictions that can exercise market power in isolated natural gas markets around the world.177 Like Alberta, these jurisdictions could reap an economic benefit from slowing their production of natural gas.

The two jurisdictions that currently have the most to gain from slower natural gas production are Texas and North Dakota. Both states are flaring vast amounts of natural gas, which means natural gas is worth zero or less at the site of the well178—that is, it would cost more to transport the gas to market than it would be worth once it got there.179 In fact, at Texas’s natural gas hub, the Waha hub, natural gas prices are often negative—that is, even if producers invest in gathering lines to take the gas from their wells to this local market, they will still have to pay to have their gas taken away.180 As a result, Texas is considering exercising its authority to cut production.181 And North Dakota’s oil and gas regulator, the North Dakota Industrial Commission, is considering limiting production as well.182 These two states have an opportunity to lead the way toward a renaissance of American state energy cartels.

III. U.S. Energy Cartels for the 21st Century

The Railroad Commission of Texas and North Dakota’s Industrial Commission should both ratchet down allowable limits of gas production to raise natural gas prices above zero in oil fields like the Permian Basin and Bakken Formation that do not have enough pipelines to carry natural gas to market. Because wells produce a mix of oil and gas, this will also mean slowing oil production down, which will also raise oil prices a bit. If properly calibrated, as in Alberta, these limits should increase immediate cash flow for operators, while extending the life of wells. The alternative methods of controlling flaring, such as flaring prohibition or fees, could devastate the industry and be environmentally counterproductive.

As long as wellhead natural gas prices are not lifted substantially above zero, stricter limits should only slightly raise delivered prices of natural gas to consumers. And it should benefit consumers by ensuring a more durable and less volatile supply of natural gas. The Interstate Oil and Gas Compact Commission can also work with Texas, North Dakota, and other oil-producing states to limit this downside by ensuring that production limits are coordinated and just enough to limit flaring, which is a waste of gas with no benefit to consumers. The overall goal should be to maximize the economic and environmental benefits from the current boom.

The reinvigorated Compact Commission can also work with the federal government to secure cooperation from other major energy exporters, such as Russia, Saudi Arabia, and the rest of OPEC. These oil and gas exporters have a shared interest in restraining production to achieve higher energy prices. Slowing global production of oil and gas will also slow emissions of greenhouse gases and other pollutants emitted by combustion of fossil fuels. This is a rare opportunity where the economic interests of key fossil fuel producers coincide with global efforts to slow carbon emissions.183 It should be seized.

A. Reforming the Railroad Commission and the Compact Commission

The Railroad Commission of Texas and North Dakota’s Industrial Commission should ratchet down gas production allowables for wells in fields with abnormal flaring until flaring returns to normal levels.184 All these wells already have allowable limits, but they are generally set above the level that any producer would reach.185 After 1973, the United States was desperate to lower oil prices, and allowables were loosened to the maximum that shared reservoirs could handle.186 And fracking obviated the need to protect shared reservoirs because each fracked well produced only the portion of the subsurface that had been fractured, rather than drawing from a larger permeable, shared reservoir.187 Freed of concern about price and shared reservoirs, for the past decade, regulators have been setting allowables so high that they do not constrain production.188 With the rise of flaring, and the collapse of oil and gas prices, it is time to ratchet down allowables again.189

There will always be some flaring in exceptional circumstances where safety or unforeseeable circumstances require it.190 But if regulators reduce production enough that natural gas prices are no longer negative at the well, industry will have an incentive to capture natural gas and bring it to market to capture that value. Industry is currently looking at many innovative ways of using natural gas, including compressing or liquefying it on the spot as well as using it to generate electricity for innovative purposes including bitcoin mining.191

Of course, fracked wells produce oil and gas together, so limits on gas production will also ratchet down oil production.192 The Commissions can limit this impact by allowing trading of gas allowables between producers so that the producers who would most benefit from maintaining current production could do so. Trading would let producers who cannot cut their gas production without cutting oil to purchase gas allowables from companies that can cut their gas production more easily.193 Alberta successfully used this kind of trading to increase the benefits of its oil production limits.194

The collateral impact of gas limits on oil production may slightly reduce revenue from oil. On one hand, reduced oil production will raise field oil prices when they are priced below world market levels because of transport constraints.195 But oil markets are better connected, so a cartel of just Texas producers usually does not exercise oil market power—that is, reducing all of Texas oil production usually will not increase the cash flow of its companies enough to offset selling less because the reduction will not have a big enough effect on world prices.196

The Texas Railroad Commission and the North Dakota Industrial Commission should start by mandating the modest level of reduction that maximizes increased cash flow from natural gas subtracting the reduced cash flow from oil.197 The Commissions could consider cutting even a bit further to maximize ultimate value of oil recovered because cutting further would reduce cash flow now but make the well produce longer.198 Of course, a dollar now is worth more than a dollar later, but Hotelling made clear that it is worth deferring sales if prices decrease faster than the appropriate discount rate.199 There is no question that natural gas, which is often worth less than zero at the well, will be worth much more in the future.200 The current rock-bottom prices for oil caused by the coronavirus mean that oil prices will also be much higher in the future—suggesting that current oil cuts could maximize the long-term value of oil and gas wells.201 Finally, the Commissions should also consider the costs to consumers and the benefits to the environment as they determine how far to cut production beyond the level that would maximize cash flow to producers.202

In the current coronavirus crisis, some oil companies have made thus far unsuccessful attempts to convince state conservation commissions to impose exactly these kind of production cuts. In Texas, two oil companies, Parsley Energy and Pioneer Natural Resources, unsuccessfully petitioned the Railroad Commission to cut oil production twenty percent to mirror the fall in “reasonable market demand” for oil.203 Similar petitions were considered in Oklahoma and North Dakota.204 The Railroad Commission rejected the petition to reduce production without a vote on May 5, 2020, suggesting it is not yet ready to impose these controls.205 One issue is that, as in the 1930s, the regulator may not yet have sufficiently complete and timely data to enforce production limits.206 On the other hand, production data is now much easier to access than it was in the past, so, given time and effort, this is a surmountable problem.207

The Interstate Oil and Gas Compact Commission should go back to its roots and assist Texas and North Dakota by working with neighboring states to moderate the pace of oil and gas development. The re-invigorated Compact Commission would be particularly helpful because the key flaring formations are both shared between two states: Texas’s Permian Basin extends into New Mexico, and North Dakota’s Bakken Formation extends into Montana.208

The Interstate Oil and Gas Compact Commission could also coordinate nationwide production of oil and gas. In 2017, the United States became a net exporter of natural gas.209 The United States is projected to be the world’s biggest exporter of liquefied natural gas in the next five years because it has a vast supply of low-priced natural gas coveted by Asian and European nations that often pay high prices for clean-burning gas.210 In theory, the United States would win more value for its gas exports if it could husband its resources for higher price periods.211 Implementing this theory, however, would require modest and time-limited production controls; producing states would only be likely to accept them if the Interstate Oil and Gas Compact Commission proved itself to be just such an adept, humble, and nimble force for coordinating state regulation.

Similarly, if it proved capable, the Compact Commission could prepare the United States for its future as an oil exporter. In December 2018, the United States became a net oil exporter.212 If it joined OPEC and Russia, together they would control sixty percent of global oil production.213 If these countries worked together, they would have more market power than any producing block since the heydays of the Compact Commission when the United States alone produced sixty percent of the world’s oil.214

B. Other Approaches to Reducing Flaring Will Not Work

State cartels are the best solution to flaring because the most commonly proposed alternative solutions have serious economic and environmental downsides. The most simple-minded solution—simply forbidding flaring—would prevent many new oil wells and create persistently negative natural gas prices that would devastate an already stressed oil industry and cause cascading releases of greenhouse gas.215 Persistently negative natural gas prices would create an affirmative incentive to flare, vent, and leak throughout the natural gas supply chain, a cascade of greenhouse gas emissions that would be even harder for regulators to control.

If oil companies cannot flare gas, they cannot drill for oil until they have built “gathering” lines that connect their proposed well to a larger pipeline that can carry it to market.216 Not only will oil companies have to invest in gathering lines; when they get to market, they will have to actually pay other companies to take their gas away.217 It makes no sense to force companies to invest in delivering a product with a negative price—the negative sign of the price indicates that it is a waste substance, the production of which harms society.218 Worse yet, as companies with oil wells are forced to deliver more and more gas to market hubs, the price of gas will become more and more negative as companies struggle to find someone willing to take the gas away.

Simple limits on flaring could also be environmentally counterproductive because persistently negative natural gas prices would encourage flaring, or worse, methane leaking, throughout the natural gas supply chain.219 And leaking is even worse for the global climate than flaring because methane is twenty-five times worse for the climate than carbon dioxide.220 Low gas prices give companies insufficient incentive to control flaring, leaking, and venting; negative prices make matters much, much worse. Every link in the chain, from well operators to gathering lines to processing plants to pipelines, would have an incentive to intentionally or accidentally leak or flare the gas rather than pay someone to take it off their hands.221

Of course, most of the parties in the gas supply chain are already subject to regulations that limit leaks and flaring, and enforcement could be stepped up, but gas leakage is already a knotty challenge for companies and regulators because a colorless, odorless gas is so hard to monitor. 222 Negative natural gas prices would destroy any incentive for companies to monitor and would turn a regulator’s job into an endless and unnecessary game of whack-a-mole with recalcitrant companies.

More moderate solutions, like banning only new flaring, or merely penalizing or taxing flaring, present the same environmental and economic problems in somewhat mitigated form. Production limits, by contrast, can attack both problems—flaring and leaking. Natural gas prices above zero will give the industry an incentive to capture, control, and sell all the gas that comes out of the ground. As venting and flaring tapers off, regulators can focus enforcement efforts on a smaller number of bad actors that are negligently wasting gas.

C. Limiting Harm to Oil and Gas Consumers

The Railroad Commission of Texas and the North Dakota Industrial Commission should start with modest limits and implement them gradually to ensure that higher natural gas prices do not harm consumers or pipeline companies. Consumers do not receive any benefit from natural gas that is flared and society as a whole loses out when a company is forced to produce a negative-value product. But raising natural gas prices too far above zero could harm end-use consumers by raising the cost of the gas they ultimately receive. It could also harm pipeline companies by eroding the geographic price differentials that allow them to profit from transporting gas. Raising prices too much could also disrupt anticipated investments in local processing and use of gas.223 At the same time, both consumers and transport companies will benefit if production limits can ensure them a longer-term supply of gas at more stable, but still low, prices.

To that end, the Railroad Commission and the Industrial Commission should not raise Permian and Bakken gas prices to anything approaching the value of natural gas at the United States’ main natural gas market—the Henry Hub in Louisiana.224 And the commissions must ensure that they do not artificially erase the differential between Henry Hub and West Texas and North Dakota prices so that there is still enough of a difference to encourage pipeline investment to bring this flood of gas to market. One lesson of the Alberta oil curtailment is that too rapid cuts can harm transport investment—Alberta later had to reduce its curtailment to correct this initial mistake.225 Texas and North Dakota should heed this lesson.

Consumers and transport companies may actually benefit if supply restrictions ensure a longer-term supply at more predictable, if initially somewhat higher, prices.226 Every time that a company builds a new factory or refinery that requires natural gas, it is making a bet on a long-term supply of affordable natural gas. The same goes for any developer that builds a new home with natural gas heating and any company that builds a new natural gas pipeline. Production limits that reduce flaring of natural gas help ensure that these customers have a long-term supply of affordable gas by conserving natural gas for the future.

D. Slowing Carbon Emissions From Oil and Gas

State cartels and a Hotelling approach to oil and gas production will slow the release of carbon dioxide that comes from burning fossil fuels.227 To maximize the long-term value of oil and gas, a coordinated global oil cartel would try to restrict supply enough to ensure that prices smoothly increase over time.228 This supply restriction would mean that, for any period, less oil and gas will be sold than would be sold in a market without collusion, limiting the greenhouse gases and other pollutants that come from burning fossil fuels. For most of the world’s major oil exporters, these externalities are unpriced, so if they coordinated to reduce production, their cooperation would produce a substantial global benefit.229

Of course, if global oil producers believed that oil consumption was going to rapidly fall to zero, there would be a much smaller benefit from coordination. Producers still might want to maximize their profit by artificially lowering prices to raise prices in the few years left to them. So, a global oil cartel would still slow oil production a bit. But there would be less value to its producers in saving oil for the future.230 But, happily, oil producers do not believe that oil consumption will rapidly decline. They see that oil consumption is higher than it has ever been, and they continue to make investments based on their belief that oil use will continue to rise.231

As a result, if other policymakers believe that oil consumption will or should fall quickly, they should urgently favor cartel formation now, while oil producers still believe that oil consumption will rise. State energy cartels are a fascinating example of a situation where differing underlying beliefs can create a strong convergence on a policy solution.232 The more oil that a producer cartel believes will be consumed in the future, the more the cartel will cut production now. And the less oil that climate regulators believe will be consumed in the future, the more important it is that oil producers cut now while they still believe otherwise.

Even if a global oil cartel would only delay production to the future, it would still have substantial benefits for climate protection. First, economic harm from climate change is often tied to the pace rather than the magnitude of warming, as communities around the world must adjust to rapidly rising temperatures.233 Second, reducing current emissions will buy us time to prepare for the worst consequences of climate change.234 Third, in the meantime, higher oil prices will benefit alternative energy sources and transportation technologies that could permanently change the trajectory of global greenhouse gas emissions.235

E. Increasing the Environmental Benefits of Natural Gas

State energy cartels can also turn U.S. natural gas production from an environmental liability to an environmental asset. Natural gas has no environmental benefit if it is vented or flared: its energy is just wasted, and it contributes to climate change by raising global concentrations of methane and carbon dioxide.236 On the other hand, if slower drilling means that gas can be shipped to markets that are currently dependent on coal for power and oil for heat, it could have significant environmental benefits. 237

Burning natural gas releases less greenhouse gas and drastically less air pollution than burning oil or coal.238 And much of the world is still dependent on oil and coal for heat and power. Coal is far and away the world’s leading source of electricity, responsible for thirty-eight percent of global power.239 And three percent of the world’s power still comes from oil, more than it gets from solar.240 Coal is particularly dominant in Asian markets that are also most affected by debilitating air pollution, and it is projected to continue rising in coming years.241 Natural gas is a particularly good replacement for coal power because, like coal and unlike solar and wind, it can produce power at any time.242 But, unlike coal, it can easily be ramped up and down, so that it allows countries to incorporate more intermittent solar and wind power into their electricity mix.243 As a result, U.S. natural gas could clean up the air in developing countries around the globe.244

If natural gas from Texas and North Dakota can reach markets around the world, it can also clean up home heating, which still often depends on coal and heating oil. China is struggling to convert millions of homes each year from coal heating to gas heating.245 Even in the United States, many households in polluted cities on the Eastern seaboard are dependent on dirtier sources such as heating oil.246 And Europe too depends on heating oil, with some countries using it to heat almost half of their homes.247 U.S. natural gas could replace these dirtier systems around the world, but only if state energy cartels can coordinate so that it is no longer flared at oil wells across the country.

Conclusion

The United States of America is emerging from history’s biggest oil boom, but it is wasting staggering amounts of natural gas and facing an uncertain future of rock-bottom oil prices. Timely action by state conservation commissions and a re-invigorated Interstate Oil and Gas Compact Commission can protect the oil industry’s health and, more importantly, conserve our resources for tomorrow’s challenges. And the federal government can leverage these actions to negotiate global cooperation on oil production that will throw its producers a lifeline and, at the same time, achieve unprecedentedly effective cooperation on slowing climate change. Texas, North Dakota, the other oil states, and the nation should move urgently and cooperatively to take this unique opportunity to protect the nation’s economy and the global environment.