This Article discusses and analyzes the proper framework for the construction of the terms “financial institution” and “financial participant” as defined in Sections 101(22)(A) and 101(22A) of the Bankruptcy Code (the Code), as they work in tandem with Section 546(e) of the Code. In 2018, the U.S. Supreme Court issued its long awaited decision in Merit, which held that the language regarding transfers “made by or to (or for the benefit of) . . . a financial institution” contained in Section 546(e) does not insulate the ultimate transferee of a constructive fraudulent action (a CFTA) simply because the company being acquired (the Target) through the leveraged buyout (an LBO) uses a bank as an intermediary between itself and its redeeming shareholders (Redeeming Shareholders). Merit stated that in such a transaction, for purposes of fraudulent transfer law and Section 546(e), the Target, not the intermediary bank, is the “transferor.” Likewise, Merit stated that the Redeeming Shareholder, as the ultimate recipient of the transfer, is the “transferee.” Merit concluded that Section 546(e) does not insulate a Redeeming Shareholder from a CFTA simply because a bank or similar entity acted as an intermediary between the Target and the Redeeming Shareholder.

Merit, however, did not address, an important issue in this context regarding the proper construction of certain language contained in Section 101(22)(A), which states that a “customer” of a financial institution will itself qualify as a “financial institution” when a financial institution, such as a bank, acts as an “agent or custodian for a customer (whether or not a ‘customer,’ as defined in section 741) in connection with a securities contract” (the Customer Language or the Customer as Financial Institution Defense). Following Merit, therefore, a large cloud of uncertainty remains as to whether a Target itself qualifies as a financial institution under the Customer Language, simply because a bank or similar entity acted as an intermediary between the Target and its Redeeming Shareholders. If the Customer Language is construed in this overly broad fashion, then essentially all Redeeming Shareholders would be insulated from CFTAs, which would make it virtually impossible for Bankruptcy Trustees to recover billions to trillions of dollars for unsecured creditors in the context of companies that file for bankruptcy within a short time period after completing an LBO or a share repurchase (or share buyback) transaction.

Courts and academics disagree on the proper construction of the Customer Language. The main misguided argument, supported by erroneous rulings of the U.S. District Court for the Southern District of New York and the Second Circuit, which drastically misconstrued the Customer Language, is that pursuant to this language a company being acquired through an LBO itself qualifies as a “financial institution,” because a bank or similar entity that functioned as an intermediary between that company and its Redeeming Shareholders acted as the company’s “agent” in the LBO, thus insulating the Redeeming Shareholders from a CFTA. The proper reading of Sections 101(22)(A) and 546(e), combined with knowledge of the securities lending industry, agency law, and the underlying policies of the Code’s “Safe Harbors,” however, belie this argument.

This Article makes the following novel argument never before raised in the academic literature regarding the interplay between Sections 101(22)(A) and 546(e): Congress inserted the Customer Language into Section 101(22)(A) to protect agent banks (Agent Banks) that act as agents for lenders in securities lending transactions (Agent SLTs). In Agent SLTs, an Agent Bank, usually a custody bank, generally holds substantial amounts of collateral for its lender-customer. Thus, in an Agent SLT, an Agent Bank generally acts as an agent and a custodian for its principal/customer—the lender of the securities. Likewise, in these transactions, the Agent Bank generally provides a guaranty to the relevant lender-customer, pursuant to which the Agent Bank agrees to indemnify the lender if the value of collateral posted by the borrower is insufficient to purchase equivalent securities to those initially loaned by the lender in the securities lending transaction (SLT) if the borrower defaults. This guaranty could be revived, making the Agent Bank liable, if after the Agent SLT is concluded: (i) the borrower files for bankruptcy; (ii) the borrower’s bankruptcy trustee later files an avoidance action such as a CFTA, and (iii) the lender becomes obligated to pay the borrower’s Trustee after either: (a) settling that avoidance action pursuant to a court-approved settlement; or (b) losing the avoidance action.

Such liability to Agent Banks could upend the securities lending market (the SLM). Indeed, absent the Customer Language, an Agent Bank generally could face significant liability in an Agent SLT because one or more of the Agent Bank’s “customers,” such as insurance companies and pension funds, may not qualify for the protection offered by the Safe Harbor contained in Section 546(e) if the borrower later files for bankruptcy. By deeming such entities “financial institutions” in a situation where an Agent Bank acts as “an agent or custodian” for its lender-customer, Congress protected Agent Banks from liability under a revived guaranty. The SLM, like the derivatives market, is an international market that involves trillions of dollars of transactions. Agent SLTs involve agent lenders that, in many situations, are “financial institutions” that act as intermediaries between their “lending” customers and the borrowers of securities. Thus, Congress did not intend the “agent or custodian” language contained in Section 546(e) to apply to garden-variety Redeeming Shareholders in LBOs, and similar transactions such as share buybacks. This interpretation of Section 101(22)(A) is consistent with the plain language of the Customer Language and with Congress’s intent in enacting, and, over the years, amending, the Safe Harbors.

This Article discusses several recent cases that have interpreted Section 101(22)(A). This Article will discuss the recent Second Circuit decision in Tribune II and argue that it was improperly decided. Likewise, this Article will discuss recent post-Tribune cases. One of those cases, Nine West, erroneously expanded Tribune II. In Greektown, however, the Bankruptcy Court for the Eastern District of Michigan disagreed with Tribune and reached an opposite conclusion—that a company being purchased through an LBO does not qualify as a financial institution under the Customer Language, simply because a bank or similar entity acted as an intermediary between the Redeeming Shareholders and the company purchased through the LBO. This Article argues that Greektown was properly decided. The Article will also discuss recent academic literature that argues that Sections 546(e) and 101(22)(A) should be construed to insulate Redeeming Shareholders of stock in publicly traded companies, but not be construed to insulate Redeeming Shareholders in nonpublicly traded companies. This Article argues that no such distinction exists under current law.

This Article makes a novel argument regarding the proper framework for the interpretation and application of Section 101(22)(A) and argues that it applies to lenders of securities in Agent SLTs that may not otherwise qualify as a customer of a broker dealer as defined in Section 741. Examples of such entities are: insurance companies, endowments, and pension funds. An understanding of the SLM combined with the text, structure, legislative history, and policy objectives of the Code readily and strongly support this conclusion.

The Article further argues that, even if courts do adopt this approach to Sections 101(22)(A) and 546(e), Congress should amend the Code so that it partially insulates shareholders in publicly traded securities, so long as those shareholders: (i) are not “insiders” of the debtor; and (ii) act in good faith.

Finally, this Article discusses and analyzes whether a debtor itself may qualify as a “financial participant” under Section 101(22A), thus insulating Redeeming Shareholders from constructive fraudulent transfer or preference liability (the Financial Participant Defense). Redeeming Shareholders have recently raised the Financial Participant Defense as an alternative to the Customer as Financial Institution Defense. Only two decisions have considered this defense, and each one of them reached opposite conclusions. This Article argues that the proper construction of the Code leads to the conclusion that a debtor itself may not qualify as a “financial participant.”

Introduction

In 2018, the U.S. Supreme Court issued its highly awaited decision in Merit Management Group, LP v. FTI Consulting, Inc.,1 which held that Section 546(e) of the Bankruptcy Code (Section 546(e)) did not prohibit a bankruptcy trustee (a Trustee) from bringing a constructive fraudulent transfer action (a CFTA) against shareholders that redeemed their shares (Redeeming Shareholders) through a leveraged buyout (an LBO), simply because a bank or other entity, which qualifies as a “financial institution” under the Bankruptcy Code (the Code), acted as an intermediary between the company acquired through the LBO (the Target) and its Redeeming Shareholders.2 Applauded by Trustees, this decision seemed to clarify a circuit split regarding the scope of Section 546(e) that had existed for over twenty years.

Merit, however, did not address a crucial issue regarding the interplay between Sections 101(22) and 546(e)—can a Target itself qualify as a financial institution by qualifying, in turn, as a “customer” of a financial institution, simply because a bank or similar entity acted as an intermediary between the Redeeming Shareholders and the Target?3 For the Target to qualify for this customer-as-financial-institution defense (the Customer as Financial Institution Defense), the bank would have to act as an “agent or custodian” for the Target in the LBO.4

In less than three years after the Supreme Court’s decision in Merit, courts have reached opposite conclusions on this issue. In 2019, the Second Circuit, in Deutsche Bank Trust Co. Americas v. Large Private Beneficial Owners (In re Tribune Co. Fraudulent Conveyance Litig.) (Tribune II), held that a trust company acting as an intermediary between a Target and its Redeeming Shareholders qualified as a financial institution because it was a “customer” of a financial institution.5 More recently, in 2020, the U.S. Bankruptcy Court for the Eastern District of Michigan, reached an opposite holding in Greektown Litigation Trust v. Papas (In re Greektown Holdings, LLC).6 Likewise, academics disagree on the proper construction of Section 101(22)(A).7 Some of those disagreements relate to the scope of the term “customer” contained in Section 101(22)(A), while others focus on the distinction between shareholders in publicly traded companies as opposed to shareholders in privately held entities (the Public vs. Private Distinction).8

In Tribune II, the Second Circuit eviscerated the Supreme Court’s holding in Merit and turned it on its head. In the short history since Tribune II, several lower courts in the Second Circuit have broadly extended its holding by, inter alia, applying Sections 546(e) and 101(22)(A) to apply to any transaction that simply involves securities.9 Such broad judicial interpretations of the customer language will result in the “exception swallowing the rule.”

If Tribune II is not soon reversed by the U.S. Supreme Court10 or by Congress, its holding will: (i) likely lead to a similar circuit split that existed for over twenty-five years prior to Merit; (ii) have a devastating impact on the ability of Trustees to successfully bring CFTAs or preference actions on behalf of general unsecured creditors against Redeeming Shareholders; and (iii) actually encourage “risky” LBOs. The following table shows the recent yearly overall volume of LBOs11:

| Year | Annual Overall Market LBO Issuance |

| 2017 | $125 Billion |

| 2018 | $150 Billion |

| 2019 | $125 Billion |

| 2020 | $84 Billion |

In addition to the Customer as Financial Institution Defense, Redeeming Shareholder defendants faced with constructive fraudulent transfer liability in the context of failed LBOs have recently raised an alternative defense, which they assert shields them from constructive fraudulent transfer and preferential transfer liability—the “Financial Participant Defense.” Specifically, these defendants have asserted that the debtor, at the time of the LBO, qualified as a “financial participant” under the Code, thus immunizing those defendants from constructive fraudulent transfer liability.12 To date, only two courts have addressed the Financial Participant Defense, with each one reaching opposite conclusions.13 As argued later in this Article, courts, in most cases, should reject this defense.

Resolution of these issues could affect the ability of future Trustees to recover literally trillions of dollars from Redeeming Shareholders on behalf of general unsecured creditors such as trade creditors, employees, and retirees. Thus, the stakes are indeed very high for current and future unsecured creditors in bankruptcies involving failed LBOs. The Covid-19 pandemic has caused, and will likely continue to cause, a large number of corporate bankruptcy filings of companies that had recently gone through an LBO or had recently engaged in share buyback transactions.14

This Article makes a novel argument never made before in the academic literature regarding the proper interpretation and scope of: (i) the term “customer” as used in Section 101(22)(A) (the Customer Language); and (ii) the term “financial participant” as used in Section 101(22A). Specifically, regarding the Customer Language (or the Customer as Financial Institution Defense), this Article argues that Congress intended the term “customer” as used in Section 101(22)(A), to protect agent banks (Agent Banks) that act as intermediaries in securities lending transactions (Agent SLTs) from liability associated with a “revived” guaranty. As discussed in more detail later, guarantees play a central role in Agent SLTs.

Indeed, as this Article describes in more detail below, absent the Customer Language, other specially defined terms contained in the Code’s safe harbors (the Safe Harbors) that define certain protected parties (each a Protected Party),15 may not apply to shield certain lenders of securities in Agent SLTs, like insurance companies, from CFTAs or preference actions. If a Trustee could successfully bring a CFTA or preference action against a securities lender in an Agent SLT months or years after an Agent SLT terminated, the Agent Bank could then face liability under a guaranty agreement (the Guaranty) to that lender for the amount the lender was required to pay the Trustee as a result of losing or settling the CFTA or preference action. As described in more detail below, it is standard market practice for an Agent Bank to give a Guaranty to the lender (the Agent Bank’s customer) in connection with an Agent SLT.

This type of exposure faced by Agent Banks’ financial market participants in Agent SLTs could lead to “systemic risk” in the financial markets, unlike the risk faced by garden-variety Redeeming Shareholders. Agent SLTs, like derivative transactions and repurchase agreements, are “specialized” transactions involving trillions of dollars, intermediaries, systemically important financial market participants, and substantial amounts of collateral. This interpretation of the Customer Language is readily and strongly supported by a combination of (i) an understanding of the mechanics of Agent SLTs and the securities lending market (the SLM); (ii) the policies underpinning the “Deep Rock doctrine” and the absolute priority rule, which are central concepts in corporate law and bankruptcy law; and (iii) the legislative history, structure, and public policy underlying the Code.

This Article will discuss basic bankruptcy concepts and the legislative intent underlying the Safe Harbors. It will also discuss the Supreme Court’s recent decision in Merit and the “financial institution” loophole that Merit left open. Next, the Article will discuss the Second Circuit’s post-Merit holding in Tribune II, along with more recent decisions, such as the U.S. District Court for the Southern District of New York’s recent decision in Nine West, which erroneously expanded Tribune II’s interpretation of the Customer Language. Likewise, the Article will discuss the recent decision in Greektown, which reached the opposite conclusion than the conclusion reached by courts in the Second Circuit.

This Article fills that void by providing an example of a transaction involving systemically important financial market participants to which the Customer Language clearly applies—Agent SLTs. The Article will provide a clear and detailed explanation of the mechanics of an Agent SLT and the systemic financial market participants involved in Agent SLTs. The Article will then argue that Congress inserted the Customer Language into Section 101(22)(A) to protect Agent Banks in connection with the role they play in Agent SLTs. The Article also argues that Congress should amend the Code, even if the Supreme Court ultimately reverses Tribune II, so that Redeeming Shareholders of publicly traded securities who do not qualify as insiders16 are partially insulated from CFTAs and preference actions if they act in good faith. Finally, this Article will argue that the Financial Participant Defense should not apply to most Redeeming Shareholders.

I. Background

A. LBOs

Decisions interpreting Section 546(e) have generally involved LBOs and Ponzi schemes.17 In the near future, such litigation may also arise with respect to transactions involving “share buy-backs,” which present similar concerns regarding Section 546(e)’s scope.18 An LBO is a merger-and-acquisition technique through which an acquirer finances the acquisition of the Target’s stock by obtaining a loan from a bank.19 The acquirer simultaneously arranges for the bank to obtain a perfected security interest in all of the Target’s assets, and it uses the loan proceeds to “cash out” the Target’s shareholders.20 There is an inherent risk involved in LBOs that the Target may later file for bankruptcy following the LBO transaction as a result of the debt incurred by the Target to pay the Redeeming Shareholders.21

B. Basic Bankruptcy Concepts

When a party files for bankruptcy under the Code, a bankruptcy estate is created.22 At that point a Trustee is appointed to administer the assets of the debtor for the benefit of the debtor’s estate—which generally means the creditors.23 The Code gives the Trustee the power to avoid or “claw back” (an Avoidance Action) various transfers of property from the recipients of such transfers that the debtor made within certain time periods prior to the Petition Date.24 Such transfers may take the form of the debtor having agreed to the: (i) granting of liens; (ii) transfer of collateral; or (iii) payment of money.

Common Avoidance Actions brought by Trustees are aimed at avoiding or “clawing back” any of the following: (i) certain prepetition liens;25 (ii) specified statutory liens;26 (iii) preferential transfers;27 and (iv) fraudulent transfers.28 The policies underlying the Trustee’s ability to bring Avoidance Actions are, inter alia, to: (i) prevent certain creditors from racing to “pick apart” the debtor’s assets on the “eve” of the debtor’s bankruptcy filing;29 (ii) prevent a debtor that shortly plans to file for bankruptcy from favoring certain creditors to the “detriment” of other similarly situated creditors;30 and (iii) prevent a debtor from depleting the assets of the estate by making “fraudulent” transfers of those assets to third parties prior to a bankruptcy filing.31 Thus, Avoidance Actions are generally geared towards the maximization of distributions to the entire body of unsecured creditors of the estate as a whole, which, in many cases, only recover a percentage of the full amount of the debt they are owed.

In essence, there are two different types of fraudulent transfer actions available to a Trustee: (i) intentional fraudulent transfer actions; and (ii) CFTAs.32 Intentional fraudulent transfers are easy to understand. An example would be a debtor gifting its property to a relative or a newly formed corporate entity before filing for bankruptcy, so that that property would not be available for distribution to its creditors.

Constructive fraudulent transfers, on the other hand, may be less obvious. A constructive fraudulent transfer occurs where a debtor, before filing for bankruptcy (i) transfers an asset for “less than a reasonably equivalent value;” and (ii) (a) is insolvent when it makes (or becomes insolvent as a result of) that transfer; or (b) was left with “unreasonably small capital” following that transfer.33 An example of a constructive fraudulent transfer would be a corporation selling one of its assets for “less than reasonably equivalent value” and either being insolvent at the time it made that sale or rendered insolvent as a result of that sale.34

Under the Code, the Trustee may bring a CFTA under (i) Section 548 of the Code (Section 548)35 and (ii) an applicable state law fraudulent transfer statute (an SLCFTA).36 Generally speaking, the important difference between CFTAs and SLCFTAs is the “look back” period that relates to the transfer the Trustee seeks to avoid. A CFTA brought pursuant to Section 548 permits a Trustee to avoid any fraudulent transfer made within two years before the debtor’s bankruptcy filing,37 while SLCFTAs generally permit a Trustee to avoid any fraudulent transfer made within a longer time period, generally four years, before the debtor’s bankruptcy filing.38

In situations involving failed LBOs, either a Bankruptcy Trustee or a trustee under a litigation trust established under a confirmed chapter 11 plan generally seeks to avoid the payments made by the debtor to the Redeeming Shareholders on a fraudulent transfer theory under either the Code39 or applicable state law40 based on either an alleged: (i) CFTA;41 or (ii) actual fraudulent transfer action.42

Fraudulent transfer law is the main avenue of recourse these unsecured creditors have to recover when a company goes through an LBO and later files for bankruptcy.43 Strong fundamental policies underpinning both corporate law44 and the Code45 support the Trustee’s power to recover payments from shareholders that redeemed their shares through an LBO on behalf of the unsecured creditors. Those policies dictate that, in the context of a bankrupt company, unsecured creditors of the corporation have priority over shareholders and that those unsecured creditors must be paid in full (or consent otherwise) before the corporation can make any distributions to its shareholders.46 In corporations liquidating outside of formal bankruptcy proceedings, the applicable doctrine is the “Deep Rock doctrine.”47 Under the Code, this priority-of-payment scheme is referred to as the “Absolute Priority Rule.”48

C. The Safe Harbors, Intermediaries & Specialized Financial Transactions

The Code insulates certain technically defined parties (Protected Parties) to certain types of financial market transactions, such as derivatives, futures contracts, and SLTs, from CFTAs and preference actions. The Code does this through the Safe Harbors, which were enacted, and significantly expanded over time.49 The Safe Harbors not only insulate Protected Parties from most Avoidance Actions, but they also exempt them from other important provisions of the Code, such as the automatic stay (the Automatic Stay) contained in Section 362 of the Code and the executory contracts provisions contained in Section 365 of the Code.50 Basically, two types of parties qualify as Protected Parties under the Safe Harbors: (i) parties that act as intermediaries (Intermediaries) in: (a) the securities and commodities clearing and settlement system (the SCCS); and (b) similar financial market transactions; and (ii) systemically important financial market participants that are parties to financial market transactions, such as parties to swap agreements, repurchase agreements, security contracts, or forward contracts.51 This narrow universe of entities enjoy this Protected Party status because their susceptibility to certain provisions of the Code could lead to systemic risk. The underlying policy of the Safe Harbors is to protect the financial markets from “systemic risk” that could result from the financial failure of a Protected Party, which, theoretically, could result if such a Protected Party were subject to most Avoidance Actions, the Automatic Stay, or certain other provisions of the Code.52

D. The Securities & Commodities Clearing & Settlement System & Intermediaries

Transactions involving publicly traded securities, commodities, and many derivatives involve various Intermediaries. In the case of publicly traded securities, parties that buy and sell securities do so through the Clearing and Settlement System.53 This system involves the use of, inter alia: (i) Intermediaries like the Depository Trust & Clearing Corporation (DTCC), stockbrokerage firms, and banks, which act as intermediaries between issuers of securities and the beneficial holders of those securities in trades involving publicly traded securities; and (ii) the use of guarantees by such intermediaries.54 Congress theorized that a domino effect of cascading bankruptcies could likely occur among large financial institutions, stock brokerage firms, clearinghouses, exchanges, or commodities dealers if a Trustee had the ability to prosecute most types of Avoidance Actions, such as CFTAs or preference actions against: (i) any one of these Intermediaries; or (ii) one of the narrowly defined systemically important financial market participants that qualifies as a Protected Party.55 As a result, Congress enacted what is now Section 546(e) in 197856 and Section 101(22) in 1984 and amended them over a twenty-one-year period.57

E. Specialized Financial Transactions

Certain specialized financial transactions such as derivative transactions, e.g., swap agreements, repurchase agreements, and SLTs are documented under forms prepared by specialized trade groups composed of major financial market participants such as the International Swaps and Derivatives Association (ISDA)58 and the Securities Industry and Financial Markets Association (SIFMA).59 These trade groups publish specific “Master Agreement” forms that are used to document such different types of specialized financial market transactions.60 This “Master Agreement” architecture allows market participants to document numerous transactions under certain pre-agreed terms contained in the market-standard Master Agreement widely used in the financial markets.61 The terms of these Master Agreements may generally be amended or tailored to a particular transaction in a schedule (Schedule) to the associated Master Agreement.62 Finally, each individual trade or transaction falling under the Master Agreement, as modified by the Schedule, is documented under a transaction or trade confirmation (a Confirmation).63

Likewise, these trade groups lobby and advocate for uniform rules that apply to the specialized financial transactions engaged in by their members. One prime area that is of grave concern to these groups is bankruptcy law. Indeed, the ability of a systemically important financial market participant to enforce certain contractual terms regarding such transactions vis-à-vis one of its counterparties that is in bankruptcy proceedings may ultimately dictate the potential recovery of billions of dollars for the nonbankrupt party to such specialized transactions, including, but not limited to, SLTs.64 The uniformity and predictability of laws applying to the SLM, commodities markets, and derivatives markets have a significant overall impact on those markets.65 Virtually all of these transactions are backed with some form of collateral (or Margin).66 Margin may consist of cash or securities.67 In the United States, transactions in the SLM are documented under securities lending agreements (SLAs), such as the Master Securities Lending Agreement (the MSLA).68

These trade groups were and are concerned with the Code’s impact on a financial market participant’s right to enforce certain terms contained in the relevant industry standard transaction forms related to, inter alia, a financial market participant’s ability to: (i) immediately terminate the relevant transaction(s); (ii) immediately realize and seize its collateral (as it can be volatile in nature); (iii) net the amounts receivable and payable under each transaction documented under the associated Master Agreement; and then determine whether: (a) the bankruptcy estate owes that market participant (i.e., the “in the money” position); or (b) the market participant owes the bankruptcy estate money (i.e., the “out of the money” position).69

Likewise, these trade groups were concerned with the ability of a Trustee to bring certain Avoidance Actions against specific financial market participants (Protected Parties) acting either as an intermediary or as a systemically important party to one of these specialized financial transactions, as such ability could result in a domino effect of bankruptcies of one or more Protected Parties, which in turn, could result in an overall meltdown of the financial markets—i.e., “systemic risk.”70 In the above types of financial market transactions, Intermediaries play central roles. Because of fears of systemic risk related to the transactions, Congress enacted, and later expanded, the Safe Harbors.

F. Section 546(e)

Section 546(e) is one of the Code’s Safe Harbors, and it limits a Trustee’s ability, in certain circumstances, to bring an Avoidance Action against certain Protected Parties such as stockbrokers, financial institutions, financial participants, and securities clearing agencies.71 Section 546(e) provides in pertinent part:

Notwithstanding sections 544, . . . 548(a)(1)(B), and 548(b) of this title, the trustee may not avoid a transfer that is a margin payment, as defined in section 101, 741, or 761 of this title, or settlement payment, as defined in section 101 or 741 of this title, made by or to (or for the benefit of) a . . . stockbroker, financial institution, financial participant, or securities clearing agency, or that is a transfer made by or to (or for the benefit of) a . . . stockbroker, financial institution, financial participant, or securities clearing agency, in connection with a securities contract, as defined in section 741(7), . . . that is made before the commencement of the case, except under section 548(a)(1)(A) of this title.72

G. Merit

Beginning in the 1990s, a circuit split, and consequent uncertainty, arose regarding the following issue: does Section 546(e) bar a CFTA against a Redeeming Shareholder simply because a bank or financial institution acted as an intermediary between that shareholder and a company in the context of an LBO of a company that later files for bankruptcy?73 In February 2018, the U.S. Supreme Court answered “no” to that question, and it unanimously held that Section 546(e) does not bar a CFTA simply because a bank or financial institution acted as an intermediary between a Redeeming Shareholder and a company in the context of an LBO of a company that later files for bankruptcy.74

Instead, Merit held that the only relevant transfer for purposes of Section 546(e) is the transfer the Trustee seeks to avoid—“the overarching [or end-to-end] transfer . . . not any component part of that transfer.”75 Thus, Merit held that, in the context of an LBO, the “transferor” for purposes of Section 546(e) was the debtor and not the intermediary bank.76 In reaching its decision, the Court looked to Congress’s intent in enacting, and later expanding, Section 546(e) of the Code, which Congress enacted in response to the Seligson77 decision to protect systemically important parties such as intermediaries in the securities and commodities clearing system.78

Merit, however, did not resolve several other issues regarding the scope of Section 546(e). Firstly, the U.S. Supreme Court, in a footnote, expressly stated that it was not deciding whether a chapter 11 debtor itself would qualify as a “financial institution” as set forth in Section 101(22)(A) by virtue of being a “customer” of an intermediary used in an LBO, such as a bank or similar entity.79 Secondly, Merit did not decide whether Section 546(e) bars a Trustee from bringing an SLCFTA.80 Thirdly, the LBO in Merit involved privately held shares of stock—it did not, like the cases that are part of the Tribune Saga81 or Nine West,82 involve publicly traded shares of stock.

Thus, following Merit, when determining whether Section 546(e) applies, a court must first look to the “overarching transfer” between the debtor (i.e., the transferor) and the Redeeming Shareholders (i.e., the transferees). If either such transferor or transferee qualifies as a “financial institution” under Section 101(22), then Section 546(e) will bar the Avoidance Action. In the short time period that has elapsed since the Supreme Court’s decision in Merit, a split among courts has already arisen regarding whether, under Section 101(22), a debtor that redeems its former shareholders’ shares through an LBO itself qualifies as a “financial institution” simply by using a bank or similar entity as an intermediary in the LBO.83 Thus, the issue that Merit seemed to have resolved has reappeared.

H. Section 101(22)

Section 546(e) gives “financial institutions” and certain other Protected Parties “special treatment”84 by insulating them from CFTAs and preference actions that a Trustee can bring under the Code.85 The underlying policy of Section 546(e) and the other Safe Harbors is to protect the financial markets from “systemic risks.”86 The term “financial institution” is defined in Section 101(22)(A).87

Congress added the defined term “financial institution” to the Code in 1984, by including it in a “Miscellaneous Amendments” subtitle of the Bankruptcy Amendments and Federal Judgeship Act of 1984.88 At that time, the definition of financial institution contained “agent or customer” language similar to the Customer Language currently contained in Section 101(22)(A).89 In 2000, Congress again amended the definition of “financial institution” by, inter alia, adding “Federal reserve bank” and the words “or receiver or conservator for such entity” into the definition.90

Approximately five years later, in 2005, Congress enacted the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA),91 which, along with significantly expanding the Safe Harbors, also amended the definition of “financial institution.” The next amendment to the definition of “financial institution” occurred approximately one year later, in 2006, when Congress enacted the Financial Netting Improvements Act (FNIA).92 Congress described this as a “technical” amendment, and it amended the Customer Language by adding the language “(whether or not a ‘customer’, as defined in section 741)” between the words “custodian for a customer” and “in connection with a securities contract.”93 The current definition of “financial institution” in Section 101(22) is:

(A) a Federal reserve bank, or an entity that is a commercial or savings bank, industrial savings bank, savings and loan association, trust company, federally-insured credit union, or receiver, liquidating agent, or conservator for such entity and, when any such Federal reserve bank, receiver, liquidating agent, conservator or entity is acting as agent or custodian for a customer (whether or not a “customer”, as defined in section 741) in connection with a securities contract (as defined in section 741) such customer; or

(B) in connection with a securities contract (as defined in section 741) an investment company registered under the Investment Company Act of 1940.94

I. Section 741

The Customer Language mentions that its definition of “customer” is not circumscribed to the definition of customer contained in Section 741, which applies in the context of liquidations of “stockbrokers.” Section 741 narrowly defines a “customer” as an:

(A) entity with whom a person deals as principal or agent and that has a claim against such person on account of a security received, acquired, or held by such person in the ordinary course of such person’s business as a stockbroker, from or for the securities account or accounts of such entity—(i) for safekeeping; (ii) with a view to sale; (iii) to cover a consummated sale; (iv) pursuant to a purchase; (v) as collateral under a security agreement; or (vi) for the purpose of effecting registration of transfer; and

(B) entity that has a claim against a person arising out of—(i) a sale or conversion of a security received, acquired, or held as specified in subparagraph (A) of this paragraph; or (ii) a deposit of cash, a security, or other property with such person for the purpose of purchasing or selling a security.95

J. Agency

Notwithstanding the inapplicability of the narrow definition of customer contained in Section 741, under the Customer Language, for an entity that is a customer of a “financial institution” to also qualify as a “financial institution,” a bank or similar entity must be acting as an “agent” or “custodian” for that customer in connection with a securities contract.96 Although the Code expressly defines “custodian,” it does not define “agent.” Thus, the common law legal definition, and not the colloquial definition, of the term agency must be determined before Section 101(22)(A) can be properly construed and applied.

An agency relationship is defined as: “[T]he fiduciary relationship that arises when one person (a ‘principal’) manifests assent to another person (an ‘agent’) that the agent shall act on the principal’s behalf and subject to the principal’s control, and the agent manifests assent or otherwise consents so to act.”97 The relationship is a legal concept and is one of “status” rather than of pure contract.98 The way the parties label their relationship “is not dispositive.”99 Therefore, a contract that simply refers to a party as an agent or labels a relationship as an agency relationship will not create an agency if the threshold elements of an agency are not satisfied.100 Indeed, it is the substance of the relationship, not the form ascribed to it in a contract, that controls.101 The finding of an agency relationship “depends on the presence of factual elements” and “[i]t is . . . a question usually reserved to the factfinder.”102

There are two bedrock principles of an agency relationship. Firstly, for an agency relationship to exist, the agent must have the power to act on the principal’s behalf, subject to the principal’s control.103 This means that the agent must have the “power . . . to bind the principal.”104 A common example of this power to bind the principal is the agent’s authority to bind the principal in a contract with a third party.105

Secondly, it is a fiduciary relationship.106 Upon formation of an agency relationship, an agent will owe the fiduciary duties of care and loyalty to its principal.107 Not every contractual relationship, however, “creates an agency relationship; in fact, most do not.”108

K. Custodian

As mentioned above, the Code expressly defines the term “custodian,” which appears alongside the term “agent” in the Customer Language. Under the Code, a “custodian” is defined as either a:

(A) receiver or trustee of any of the property of the debtor, appointed in a case or proceeding not under this title;

(B) assignee under a general assignment for the benefit of the debtor’s creditors; or

(C) trustee, receiver, or agent under applicable law, or under a contract, that is appointed or authorized to take charge of property of the debtor for the purpose of enforcing a lien against such property, or for the purpose of general administration of such property for the benefit of the debtor’s creditors.109

II. Recent Cases Interpreting Section 101(22)(A)

A. The Tribune Saga

The Tribune saga began with the issue of whether Section 546(e) preempted SLCFTAs in the context of LBOs.110 Later, in addition to that issue, it addressed, although incorrectly, one of the major issues regarding Section 546(e) that Merit did not resolve111—whether the debtor itself would qualify as a financial institution by virtue of being a “customer” of an entity that acted as an intermediary in the LBO, such as a bank or trust company.112 Such an interpretation of Sections 101(22)(A) and 546(e) in the context of LBOs would not only give corporate insiders a defense that is “too good to be true,”113 but it also would immunize virtually every Redeeming Shareholder in the context of a failed LBO from constructive fraudulent transfer liability.114

1. Tribune I

In 2016, the Second Circuit issued a decision that held that, in the context of an LBO involving an intermediary bank or trust company, Section 546(e) of the Code prevented a Trustee from bringing SLCFTAs and CFTAs against Redeeming Shareholders.115 Around this time, in Physiotherapy,116 the U.S. Bankruptcy Court for the District of Delaware reached the opposite conclusion, and held that Section 546(e) did not preempt SLCFTAs in the context of LBOs.117 The plaintiffs in Tribune I later filed a petition for certiorari regarding the Tribune I decision to the U.S. Supreme Court.118 The U.S. Supreme Court held several conferences on that petition for certiorari. During that time period, the U.S. Supreme Court issued its holding in Merit. Following the Court’s decision in Merit, on April 3, 2018, Justices Kennedy and Thomas issued a statement suggesting that, in light of Merit, the Second Circuit recall its mandate.119 As discussed in more detail below, the Second Circuit did recall its mandate, and later, it issued its amended erroneous decision in Tribune II.120

2. Tribune Customer Case

Following Merit, but before the Second Circuit issued Tribune II, the District Court for the Southern District of New York in the Tribune Customer Case issued a decision interpreting Section 101(22)(A), which defines “financial institution.”121 Based on the holding in Merit, the trustee representing a group of individual creditors (the Tribune Trustee) sought to amend his complaint so that he could bring a CFTA against certain shareholders that redeemed their shares through the LBO of the Tribune Company (Tribune).122 The District Court for the Southern District of New York denied that motion and held that, notwithstanding Merit, Section 546(e) would immunize Tribune’s shareholders from a CFTA because Tribune qualified as a “financial institution” under Section 101(22)(A).123

According to the district court’s faulty construction of the Code and agency law, a trust company, Computershare Trust Company, N.A. (CTC), qualified as Tribune’s “agent” in the challenged transaction simply by agreeing to collect and cancel the shares of former Tribune shareholders that cashed out their shares through Tribune’s LBO.124 According to the district court, under the definition of “financial institution” in Section 101(22)(A), CTC’s purported role as Tribune’s “agent” rendered Tribune itself a “financial institution.”125 The district court did not cite a single case for the proposition that combination entrustment and payment constitutes “a paradigmatic principal-agent relationship.”126

3. Tribune II

In December 2019, the Second Circuit issued its amended opinion in Tribune II, concluding, as it did in Tribune I, that Section 546(e) preempts SLCFTAs.127 Much of Tribune II contained the same reasoning as Tribune I. Like Tribune I, the Tribune II court repeated its concern that subjecting investors in publicly traded equity securities to constructive fraudulent transfer liability may weaken investor confidence in the public security markets.128 Tribune II, however, implemented essentially the same erroneous reasoning Judge Cote used in the Tribune Customer Case regarding whether Tribune itself qualified as a “financial institution” as set forth in Section 101(22)(A).129 In Tribune II, the Second Circuit ultimately concluded that: (i) CTC qualified as Tribune’s “agent” in the LBO simply by agreeing to act as an intermediary between Tribune and its shareholders; and (ii) CTC’s role as Tribune’s “agent” rendered Tribune itself a “financial institution” pursuant to the definition of financial institution set forth in Section 101(22)(A).130 As described in more detail later in this Article, the Second Circuit’s ruling in Tribune II was erroneous, because, inter alia, it misconstrued: (i) Section 101(22)(A); (ii) the nature of most relationships between banks and their customers; and (iii) agency law.131

On July 6, 2020, the Tribune Trustee filed a petition for certiorari (the Tribune Petition) to the U.S. Supreme Court.132 On October 5, 2020, the U.S. Supreme Court requested that the U.S. Solicitor General file a brief regarding the Tribune Petition.133 On March 12, 2021, the U.S. Solicitor General filed her brief, in which she agreed with many arguments made by the Tribune Trustee, but nevertheless argued that the U.S. Supreme Court deny the Tribune Petition because, other than the Second Circuit, “[n]o other circuit has addressed whether, or under what circumstances, a party may qualify as a ‘financial institution’ for purposes of Section 546(e) simply by retaining a bank (or similar entity) to help effectuate a securities transaction.”134 On April 19, 2021, the U.S. Supreme Court denied the Tribune Petition.135

Although Tribune II’s erroneous decision currently applies in the Second Circuit, courts in other circuits may easily reach an opposite conclusion, giving rise to a circuit split and another possibility for the U.S. Supreme Court to decide the issue. Indeed, as described in more detail below, in Greektown, the U.S. Bankruptcy Court for the Eastern District of Michigan, finding Tribune II’s reasoning unpersuasive, recently did so.136 Ideally, Congress would soon amend Section 546(e) as suggested later in this Article. Congress, however, is unlikely to do so any time soon because of, inter alia, the number of politically divisive issues currently beleaguering Congress. In the meantime, courts in circuits outside of the Second Circuit should not follow Tribune II’s erroneous holding. Instead, they should follow the sound reasoning of Greektown, which properly interpreted Section 101(22)(A).

B. Nine West

A recent decision from the Southern District of New York expanded the holding of Tribune II in the context of LBOs in a case stemming from the bankruptcy filing of Nine West Holdings, Inc.137 In Nine West, the district court held that Section 546(e) insulated all transfers made to a debtor’s entire body of Redeeming Shareholders in an LBO from, inter alia, an SLCFTA138 simply because the predecessor company of debtor, Nine West Holdings, Inc. (NWHI),139 and its parent company, Jasper Parent LLC (Jasper Parent), entered into a contract with Wells Fargo, N.A. (Wells Fargo) under which Wells Fargo acted as an intermediary between NWHI and a small, distinct set of its shareholders involving only a minuscule portion, or 0.4%, of the entire LBO.140

In Nine West, payments to the Redeeming Shareholders were made in three separate ways.141 Specifically, Jasper Parent: (i) deposited approximately $4 million with Wells Fargo so that shareholders holding paper stock certificates could receive payment on account of their cancelled shares (the Certificate Transfers);142 (ii) deposited approximately $1.105 billion into an account at Wells Fargo, which Wells Fargo agreed to wire to the DTCC, which in turn, credited the accounts of broker-dealers in favor of other shareholders of the debtor (the DTCC Transfer); and (iii) paid $78 million to insider and employee shareholders of the debtor through NWHI’s payroll system.143

The district court specifically found that Wells Fargo was NWHI’s agent only with respect to the Certificate Transfers.144 The district court, however, went on to erroneously hold that once Wells Fargo was found to be an agent with respect to any transfer connected to the LBO, here the Certificate Transfers, it qualified as an agent of NWHI so that Section 546(e) would insulate all transfers made in connection with the LBO from avoidance, including (i) the DTCC Transfer, in which Wells Fargo had an extremely limited nonagent role; and (ii) the Payroll Transfer, in which Wells Fargo played no role whatsoever!145

C. Greektown

In October 2020, the Bankruptcy Court for the Eastern District of Michigan (Judge Oxholm) issued an opinion that reached the opposite conclusion that Tribune II reached.146 Greektown involved the following facts. Two separate LLCs, Monroe Partners, LLC (Monroe)147 and Kewadin Greektown Casino, LLC (Kewadin), each owned fifty percent of the membership interests in Greektown Holdings, LLC (Greektown Holdings).148 Kewadin agreed to purchase the membership interests of Monroe’s prior members (the Prior Monroe Members) by making future periodic payments to them. Kewadin financed this transaction by causing Greektown Holdings to enter into an LBO.149

Pursuant to the LBO, Greektown Holdings borrowed approximately $182 million from Merrill Lynch, Pierce Fenner & Smith Inc. (Merrill Lynch).150 Greektown Holdings did this by issuing notes to Merrill Lynch, which, pursuant to a Note Purchase Agreement and related documents (collectively, the Transaction Documents), acted as, inter alia, the sole lead administrative agent for the notes.151 Pursuant to the Transaction Documents, Merrill Lynch was able to resell all or a portion of the notes to other institutional investors.152 Merrill Lynch wired approximately $170 million from the proceeds of the sales of the notes to the bank accounts of the Prior Monroe Members.153 Approximately two years and six months later, Greektown Holdings filed for chapter 11.154 Later, a litigation trustee appointed under Greektown’s confirmed chapter 11 plan sought to avoid, on behalf of Greektown’s unsecured creditors, approximately $155 million in payments made to the Prior Monroe Members by asserting, inter alia, an SLCFTA.155

The Prior Monroe Members moved for summary judgment, arguing that Section 546(e) barred the action.156 Like the defendants in the Tribune Customer Case, Tribune II, and Nine West, the Prior Monroe Members argued that Greektown Holdings itself qualified as a “financial institution” because Merrill Lynch, a bank, acted as Greektown Holdings’ “agent” in the LBO by being an intermediary between the Prior Monroe Members and Greektown Holdings in the LBO.157 The bankruptcy court correctly rejected this faulty argument and denied the motion for summary judgment.158 In so doing, the court analyzed the plain language of Section 101(22)(A), agency law, and the Transaction Documents.159

2. Greektown’s Analysis of Merit and Section 546(e)

The court analyzed Merit, noting that Merit held that, for purposes of Section 546(e), “the only relevant transfer . . . is the transfer that the trustee seeks to avoid.”160 The court then explained how in Merit, the Supreme Court held that, when the trustee seeks to avoid a transfer, the transfer to be avoided is the transfer from the transferor to the ultimate transferee, and not the transfer to or from any intermediary acting between the transferor and the ultimate transferee.161 Stated differently, the court correctly noted that Section 546(e) does not immunize a transfer from avoidance simply “because a qualified intermediary acted as a conduit between the debtor and the transferee.”162

The court noted that, in Merit,

the Supreme Court determined that . . . “the relevant transfer for purposes of the [Section] 546(e) safe-harbor inquiry is the overarching transfer that the trustee seeks to avoid.” . . . In so ruling, the Supreme Court emphasized that [Section] 546(e) is a limitation on an otherwise avoidable transfer[.] The transfer that . . . “the trustee may not avoid” is specified to be “a transfer that is” either a “settlement payment” or made “in connection with a securities contract.” Not a transfer that involves. Not a transfer that comprises. But a transfer that is a securities transaction covered under [Section] 546(e).163

Moreover, the court noted that Merit accentuated the underlying legislative intent of Section 546(e)—to protect Qualified Intermediaries.164 The court stated:

Congress was concerned about transfers “by an industry hub” specifically: The safe harbor saves from avoidance certain securities transactions “made by or to (or for the benefit of)” [Qualified Intermediaries]. . . . Transfers “through” a [Qualified Intermediary], conversely, appear nowhere in the statute. And although Merit complains that, absent its reading of the safe harbor, protection will turn “on the identity of the investor and the manner in which it held its investment,” that is nothing more than an attack on the text of the statute, which protects only certain transactions “made by or to (or for the benefit of)” certain covered entities.165

The court, again pointing to Merit, stated that the relevant transfer was the transfer from Greektown Holdings to the Prior Monroe Members—“the transfer the trustee sought to avoid.”166 The court then analyzed the “for the benefit of” language of Section 546(e) and determined that although Merrill Lynch earned substantial profits for its role in the LBO, the Prior Monroe Members failed to establish “that Merrill Lynch received a direct, ascertainable, and quantifiable benefit corresponding in value to the payments to [the Prior Monroe Members].”167 The court stated that the advisory fees and other fees Greektown Holdings paid to Merrill Lynch for its role in the LBO were “not the type of benefit contemplated by the phrase ‘for the benefit of,’” but were merely “incidental to the [LBO].”168 The court noted that the “for the benefit of” language applies to a situation where there is a “benefit to a guarantor by the payment of the underlying debt of the debtor.”169

3. Greektown Properly Concludes that Merrill Lynch Failed to Qualify as Greektown’s Agent in the LBO

The court then analyzed whether Greektown Holdings itself qualified as a financial institution by, in turn, analyzing whether “Merrill Lynch was acting as an agent” of Greektown Holdings in the LBO.170 The court pointed to the definition of agency.171 The court further noted that the comments to the Restatement (Third) of Agency explain that not every party that functions as an intermediary between two other parties qualifies as an agent.172 Likewise, the court noted that the principal’s “right to control the conduct of the agent” is “fundamental to the existence of an agency relationship.”173

After analyzing the Transaction Documents, the court held that Merrill Lynch did not act as Greektown Holdings’ agent or custodian in the LBO.174 The court further stated that it was “not persuaded by the agency analysis in [Tribune II] as it does not distinguish between mere intermediaries contracted for the purpose of effectuating a transaction and agents who are authorized to act on behalf of their customers in such transactions.”175 The court noted that Tribune II held that Tribune had control over the intermediary involved in its LBO “by merely authorizing Computershare to accept funds as part of the [LBO] and further effectuating the transaction.”176

The court further noted that Tribune II did not analyze the transaction documents between Tribune and Computershare in reaching its conclusion that Computershare acted as Tribune’s agent in the LBO, making it impossible to establish whether the language contained in those transaction documents was similar to the Transaction Documents involved in Greektown Holdings’ LBO.177 The court also noted that the holding in Tribune II would lead to the conclusion that “any intermediary hired to effectuate a transaction would qualify as its customer’s agent,” thus “result[ing] in a complete workaround of Merit Management, which opined that the safe harbor provision does not insulate a transfer simply because a qualified intermediary acted as a mere conduit.”178

Looking to the Transaction Documents, the court noted that, although Merrill agreed to “arrange an offering of senior unsecured notes . . . to act as exclusive financial advisor to . . . [Greektown Holdings] in connection with exploring Strategic Alternatives,” it did not agree to act as Greektown Holdings’ agent.179 The Transaction Documents, however, stated that “Merrill Lynch shall act as an independent contractor.”180 More importantly, however, the Note Purchase Agreement181 executed between Merrill Lynch and Greektown Holdings expressly provided that: (i) Merrill Lynch was “acting solely as principals and [we]re not the agents or fiduciaries of [Greektown Holdings;]” and (ii) Merrill Lynch did not have any “obligation[s]” to Greektown Holdings with respect to the LBO other than the “obligations expressly set forth in [the Note Purchase Agreement].”182

Next, the court analyzed the credit agreement (Credit Agreement),183 which expressly provided that “[e]ach Lender [i.e., each note purchaser] hereby designates [Merrill Lynch] to act as the Administrative Agent under [the Transaction Documents] and authorizes [Merrill Lynch], in its capacity as the Administrative Agent, to act on behalf of such Lender under [the Transaction Documents].”184 The Credit Agreement further provided that Merrill Lynch accepted its role as Administrative Agent for the other note purchasers and that the note purchasers authorized Merrill to act as their agent.185 The Credit Agreement also stated that Merrill Lynch would not have “any right, power, obligation, liability, responsibility or duty under [the Transaction Documents] other than those” that apply to Merrill Lynch “in its capacity as a Lender” pursuant to the Transaction Documents.186 Moreover, the Credit Agreement provided that Merrill Lynch would not have any “fiduciary relationship with any Lender.”187

The court held that no agency relationship existed between Greektown Holdings and Merrill Lynch.188 The court concluded that Merrill Lynch’s collection and distribution of the loan proceeds pursuant to its agreement with Greektown Holdings was not sufficient to establish that Greektown Holdings “controlled” Merrill Lynch in the LBO to give rise to an agency relationship.189 Instead, the court concluded that Greektown Holdings “merely authorized [Merrill Lynch] to perform contractual services.”190 The court further stated:

The [Transaction Documents] do not establish that [Merrill Lynch] was “a business representative” or could “bring about, modify, affect, accept performance of, or terminate contractual obligations between Holdings and third persons.” . . . In fact, [Merrill Lynch] was on the other side of the transaction ([Greektown] Holdings as issuers and [Merrill Lynch] as purchaser; [Greektown] Holdings as borrower and [Merrill Lynch] as lender).191

Instead, the court found that under the Transaction Documents, Merrill Lynch acted as an agent for the other lender/note purchasers, which were on the opposite side of the transaction from Greektown Holdings.192 The court then held that Merrill Lynch did not qualify as a custodian of Greektown Holdings. The court indicated that the Prior Monroe Members did not have any lien on the proceeds of the note sales.193 Likewise, Merrill Lynch was not: (i) enforcing any such lien;194 or (ii) administering any property “for the benefit of all” of Greektown Holdings’ creditors.195

As analyzed in more detail below, Greektown properly construed Section 101(22) as it acts in tandem with Section 546(e). But that begs the question—why did Congress use the following language (the Customer Language) in Section 101(22)(A): “when any such Federal reserve bank, receiver, liquidating agent, conservator or entity is acting as agent or custodian for a customer . . . in connection with a securities contract . . . such customer.”196 Indeed, as mentioned above, much of that language was contained in the original definition of “financial institution,” which Congress added to the Code in 1984.197 There is one type of transaction, however, involving systemically important parties, to which the application of the Customer Language makes perfect sense—Agent SLTs, which involve agent banks.

III. Securities Lending and the Securities Lending Market

A. Basics of SLTs

Recall that Section 546(e) was enacted to protect Protected Parties, which generally act as: (i) Intermediaries; or (ii) systemically important financial market participants in certain specialized financial transactions whose susceptibility to certain provisions of the Code could cause “systemic risk” in the financial markets. In connection with LBOs, Section 546(e) should act to protect only the Code’s narrowly defined Protected Parties, which are systemically important financial market participants, such as a bank acting as an intermediary in an LBO or an entity acting as an intermediary in the SCCS. Furthermore, although some of the transaction documents with banks or similar intermediaries involved in LBOs may qualify as a securities contract, those are not the only types of “securities contracts” to which “financial institutions” are parties. Another type of securities contract is a contract associated with the lending of securities, taking collateral, and issuing a Guaranty with respect thereto—i.e., documents used in Agent SLTs.198 Securities contracts that are associated with Agent SLTs are routinely entered into by banks, stockbrokers, and other systemically important interconnected financial market participants in the SLM.199

The SLM is a worldwide business, which as of 2019, had a total estimated loan balance of over $800 billion.200 The major “players in the [SLM] are securities houses, investment banks, fund managers, pension funds, central banks, insurance companies, broker dealers, hedge funds,” and large corporations containing a significant amount of treasury stock.201 SLTs may be structured on either: (i) an “on demand” basis;202 or (ii) a “term basis”—i.e., for an agreed-upon period of time.203 The SLM is vitally important to both the international and the U.S. financial markets. For example, virtually every transaction involving a “short sale” of a security involves an SLT.204 Likewise, many “prime brokerage” transactions involve an SLT.205

Basically, an SLT functions as follows. The lender of the securities lends those securities to a borrower.206 The borrower, in return, posts Margin to the lender, which generally takes the form of cash or securities.207 Even though terms such as “borrower,” “lender,” and “collateral” are used, documents used in the SLM generally treat the “loan” of the securities from the lender to the borrower as an “outright transfer” of lender’s title to those securities to the borrower.208 Likewise, SLAs generally treat the transfer of Margin from the borrower to the lender as an “outright transfer” of the borrower’s title in that Margin to the lender.209 This allows the “borrowed securities” and the Margin to either be sold or lent to other market participants by the borrower or the lender, as the case may be.210 At the agreed-upon conclusion date of the transaction (the Maturity Date), the borrower has the obligation to return equivalent securities (Equivalent Securities) to the lender that the lender had lent to it, and the lender has the concurrent obligation to return the Margin to the borrower.211

Various interconnected intermediaries play a central role in the SLM, such as: (i) custody banks; (ii) prime brokers; (iii) banks; and (iv) clearinghouses and central securities depositories.212 Custody banks generally “lend securities from the portfolios they hold on behalf of institutional investors.”213 Prime brokers, on the other hand, generally grant “access to lendable securities” to hedge funds, which are clients of the prime broker.214 Clearinghouses and central securities depositories “clear and settle securities [transactions] and provide a number of automated services such as stock identification and tracking.”215 Large central securities depositaries settle most SLTs.216 As a leading publication often consulted by attorneys and market participants engaging in SLTs explains:

Intermediaries typically provide valuable services such as supplying liquidity, i.e. borrowing securities on demand and lending them on a term basis. They also offer credit enhancement and comprehensive administrative services covering mark to market calculations (advised to both the borrower and lender), checking collateral eligibility and managing it, custody of securities, inter account transfers, dealing with dividends and other corporate actions, daily reporting and protecting borrowers from recalls.217

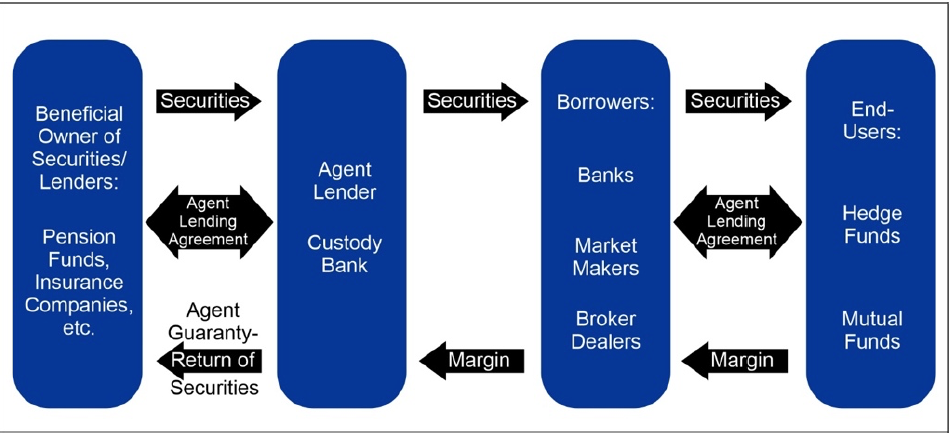

B. Agent SLTs

Agent SLTs generally involve an Agent Bank, which is usually a custody bank, that acts as an agent for its “principal” and “customer,” the securities lender, when the securities lender loans securities to a third party typically involved in Agent SLTs, such as registered broker-dealers.218 That broker-dealer, in turn, loans those securities to various borrowers such as hedge funds or mutual funds.219 This agency relationship between the lender of the securities and the Agent Bank is a fiduciary relationship, in which the lender is the principal and the Agent Bank is the agent.220 In such transactions, the lenders are the “customers” of the Agent Bank and are generally institutional investors such as: central banks, sovereign wealth funds, pension funds, endowments, insurance companies, or large corporations containing a significant amount of treasury stock.221

Agent SLTs generally involve the following agreements: (i) an agreement executed between the agent and its customer/lender that describes, inter alia, the terms of the agent-lending arrangement;222 and (ii) an agreement that contains the terms applicable to the lending arrangement and the roles of the parties involved in the transaction.223 In Agent SLTs, the lender profits by charging a fee to the borrower.224 The Agent Bank, on the other hand, profits through a fee agreement with the lender, which is usually an agreed-upon “fixed percentage split of the income generated by the lending activity and the reinvestment of [the Margin].”225

The Agent Bank generally carries out the following activities: (i) receiving requests from prospective borrowers and deciding whether to make the loan; (ii) transferring the loaned securities to the borrower’s account, and (iii) collecting the Margin from the borrower and crediting it to the lender’s account, which is also maintained with the Agent Bank.226 The Agent Bank also monitors the value of the Margin on a daily basis.227 If the value of the Margin falls below a pre-agreed upon amount, the Agent Bank will generally make a call for additional Margin from the borrower.228 On the Maturity Date, the Agent will: (i) transfer the Equivalent Securities to the lender’s account; and (ii) transfer the Margin to the borrower’s account.229 Thus, in Agent SLTs, the Agent Bank may act as both an agent for a lender and as a custodian of the Margin.230

An Agent Bank, similar to an intermediary in the SCCS, provides an indemnity or Guaranty to its customer (i.e., its principal—the securities lender), pursuant to which the Agent Bank agrees to indemnify the lender in an event of a borrower default (a Borrower Default)—which would occur if, inter alia, the value of the Margin posted by the borrower is insufficient to purchase Equivalent Securities on the Maturity Date.231

If a Borrower Default occurs, the Agent is generally obligated to liquidate the Margin and use the proceeds thereof to buy Equivalent Securities.232 If the liquidation of the Margin does not produce sufficient proceeds to purchase those Equivalent Securities, then the Agent, under the Guaranty or the indemnity, is obligated to use its own funds “to make up the difference” between amount realized by the liquidation of the Margin and the amount required to purchase the Equivalent Securities.233

A diagram of the transaction may look like this234:

C. Insolvency Concerns Related to Agent SLTs

As mentioned above, one of the major concerns for financial market participants engaging in specialized financial transactions involving systemically important parties, such as swap agreements, repurchase agreements, forward contracts, and SLTs, is their ability to enforce certain rights contained in the applicable transaction documents if a counterparty to such a transaction files for bankruptcy.235 In the case of SLTs,236 some of those bankruptcy-related concerns are: (i) the ability to net various securities lending transactions documented under a MSLA or similar master agreement against each other to arrive at a net amount;237 (ii) the ability to promptly liquidate the Margin and apply the associated proceeds thereof to the debtor’s obligations; (iii) the lender’s vulnerability to an Avoidance Action238 asserted by a Trustee of the borrower’s bankruptcy if the Agent, at an earlier time, liquidated the Margin and transferred the proceeds to that lender; (iv) in the situation of such an Avoidance Action, the ability of the Guaranty to be revived, making the Agent liable to the lender for the amount paid by the lender to the Trustee.239

IV. The Proper Framework for Interpreting and Applying the Customer Language Contained in Section 101(22)(A) Is that It Applies to Agent SLTs, Not LBOs

A. Congress Enacted Section 101(22)(A) to Insulate Agent Banks in Agent SLTs from Liability Associated with a Revived Guaranty

Recall that Section 546(e) prevents a Trustee from bringing a CFTA or preference action against a Protected Party if the transfer was made pursuant to a Safe Harbor transaction.240 When a Trustee brings a CFTA or a preference action, the Trustee generally sues the “transferee” of property it is seeking to recover.241 Generally, an intermediary is not considered a “transferee” under the Code, because an intermediary does not have a beneficial interest in the property it received from the debtor.242 Instead, an intermediary receives that property in a bailee-like capacity, on behalf of the beneficial owner.243 As mentioned above, the Court in Merit recognized this concept in its holding.244

As mentioned in more detail earlier in this Article, the Safe Harbors were enacted to prevent “systemic risk” in the financial markets by preventing a “domino effect” if either an intermediary in the SCCS or one of the Code’s narrowly defined Protected Parties245 filed for bankruptcy. Many, if not all, of the financial market participants in Agent SLTs, such as Agent Banks, stockbrokers, and mutual funds, generally qualify for status as one of these narrowly defined Protected Parties, such as a financial participant, stockbroker, or the “catchall” category of a “financial institution.” Thus, these systemically important financial market participants would be immune to a CFTA or a preference action. This catchall category of financial institution is especially important in Agent SLTs.

As described above, Agent Banks play a crucial role in the SLM. If a borrower in an Agent SLT files for bankruptcy, the Trustee of the borrower’s bankruptcy estate could bring a CFTA (or preference action) against the securities lender, seeking to claw back the value of the Equivalent Securities (or the related Margin) the debtor transferred, through the Agent Bank, to the securities lender—the transferee. The Agent Bank would most likely either: (i) not qualify as a transferee under the Code because it functioned solely in the capacity of an intermediary; or (ii) qualify as one of the Code’s narrowly defined Protected Parties.246 Certain lenders of securities however, such as endowments, insurance companies, or pension funds, may not qualify as either: (i) one of those Protected Parties; or (ii) an intermediary.

Although Agent Banks will generally qualify as either an intermediary or a Protected Party, if Section 101(22)(A) did not contain the Customer Language, neither status as an intermediary nor as a Protected Party would protect an Agent Bank from potential significant liability to the securities lender resulting from a “revived” Guaranty.247 The Guaranty could be revived if: (i) the borrower returned Equivalent Securities to the securities lender on the Maturity Date; (ii) the borrower later filed for bankruptcy; (iii) the Trustee of the borrower’s bankruptcy estate later brought a CFTA (or preference action) against the securities lender (i.e., the customer of the Agent Bank), seeking to claw back the value of the Equivalent Securities (or the related Margin);248 and (iv) the Trustee is successful in either: (a) obtaining a judgment against the securities lender;249 or (b) negotiating a court-approved settlement of such an Avoidance Action.250 This situation creates credit risk for the Agent Bank.251 In this situation, an Agent could face significant losses, making it unable to complete other SLTs.

The bankruptcy filings of several borrowers in Agent SLTs would exacerbate this risk. Such numerous borrower bankruptcy filings, in turn, could cause defaults by other parties to SLTs, resulting in “systemic risk” or a “domino effect” of Agent Banks and other systemically important financial market participants that are crucial to the effective functioning of the SLM.252 Indeed, this hypothetical scenario gives rise to similar bankruptcy-related concerns that arose as a result of Seligson, which, as Merit explained, caused great concern among financial market participants in the SCCS, a central and integral part of the overall financial markets.253

As mentioned above, such concerns led to the enactment and eventual expansion of the Safe Harbors.254 Thus, by insulating an Agent Bank’s “customer” (the securities lender in an Agent SLT, such as an insurance company or an endowment that may not otherwise qualify as a Protected Party) from constructive fraudulent transfer or preference liability, Congress prevented the rise of such contingent Guaranty liability in the first place. Without such liability, Agent Banks, which are systemically important financial market participants, could not have any liability on a revived Guaranty triggered by a Trustee having brought a preference action or a CFTA against a securities lender in an Agent SLT.

The Customer Language contains the following language relating to certain defined parties that act as “an agent or custodian” for a “customer”: “when any such Federal reserve bank, receiver, liquidating agent, conservator or entity is acting as agent or custodian for a customer (whether or not a ‘customer’, as defined in section 741) in connection with a securities contract (as defined in section 741) such customer.”255

An Agent SLT is truly a fiduciary relationship—i.e., an agency relationship, where the Agent Bank is the agent of the lender, which is also the principal.256 If Congress did not insert the Customer Language in Section 101(22)(A), Agent Banks could face significant losses stemming from a revived Guaranty, that in turn, resulted from a lender’s (i.e., the customer of the Agent Bank) loss or settlement of a CFTA or preference action. This seemingly convoluted Customer Language deems a securities lender in an Agent SLT to fit within the catchall definition of a “financial institution,” and thus the securities lender qualifies as a Protected Party against which a Trustee could not bring a CFTA or a preference action. As a result, an Agent Bank is insulated from liability related to a revived guaranty triggered by a CFTA (or preference action) brought against the Agent Bank’s customer—the securities lender.

B. “Customer” Definition Contained in Section 741

Congress’s inclusion of the parenthetical, “(whether or not a ‘customer’, as defined in Section 741),” within the Customer Language supports this construction of Section 101(22)(A).257 The definition of “customer” contained in Section 741 is limited in scope and applies to liquidations of broker-dealers (Stockbrokers).258 The definition of “customer” under Section 741, and under the Securities Investor Protections Act (SIPA), are: (i) very similar to one another;259 and (ii) “narrowly defined.”260

Stockbrokers cannot file for chapter 11 bankruptcy protection,261 but they can, however, file for bankruptcy under subchapter III of chapter 7 of the Code.262 Similarly, if the Stockbroker is a registered broker-dealer, which most of them are,263 the Stockbroker could be subject to a proceeding under SIPA, which incorporates many of the provisions of the Code into SIPA.264 Thus, many of the cases construing the definition of “customer” under Section 741 have arisen in SIPA cases.265

Congress enacted SIPA to boost public investors’ confidence in the securities markets and to fortify the financial responsibility of Stockbrokers to eliminate, to the extent possible, risks leading to customer losses.266 One of the principal risks SIPA seeks to avert is the possible domino effect of insolvencies to other financial market participants that the insolvency of a Stockbroker could cause.267 Thus, SIPA, like the Safe Harbors, seeks to minimize “systemic risk” in the financial markets that could result from the insolvency of a party that is often central to financial market transactions—in the case of SIPA, that party is a Stockbroker. To meet this goal, SIPA created the Securities Investor Protection Corporation (SIPC), a nonprofit corporation whose members consist of most broker-dealers.268

SIPC administers a fund (the Customer Fund)269 financed from mandatory contributions of its member-brokers, to be used for the purpose of reimbursing “customers” of such a Stockbroker (the Stockbroker Customers) that suffer losses caused by a Stockbroker’s insolvency.270 Once a determination is made that a Stockbroker is on the verge of insolvency, SIPC may request that a court determine that SIPA applies for the benefit of the “customers” of the failed Stockbroker.271 Those that qualify as Stockbroker Customers have priority over the other general unsecured creditors of the failed Stockbroker, and, in the case of a SIPA proceeding, have the right to take from the Customer Fund.272