Revlon, the well-known cosmetics manufacturer, has labored under a massive debt load since the 1980s, when it was the subject of a classic hostile takeover battle. As with many recent distressed firms, it decided to address its debt not through the Bankruptcy Code and chapter 11, but rather in an “exchange offer.” That is, it offered to buy its old bonds back with an offer of new securities. One implication of its decision to proceed this way was that it was able to pay its retail bondholders much less than its institutional bondholders.

The Trust Indenture Act of 1939 was supposed to protect small bondholders from abuse by issuers and their fellow bondholders. Nevertheless, recent exchange offers have become more aggressive than ever. And academic scholarship has argued that the Trust Indenture Act should be repealed because, allegedly, there are very few individual bondholders anymore.

Leaning against this ancient and illustrious literature, I instead argue that today we need the Trust Indenture Act, and Section 316(b) thereof, more than ever. Indeed, I argue for an expansion of the Trust Indenture Act to provide more robust protection for small bondholders, the disappearance of which I submit has been seriously overstated.

I argue that the Trust Indenture Act should be viewed as a floor, from which Securities and Exchange Commission rulemaking can further develop to animate the spirt of the Trust Indenture Act. In particular, by adapting key concepts from equity tender offers—like the “best price” and “all holders” rules—exchange offers can be made more equitable. In addition, I propose a new two-stage process for exchange offers, which exposes tendering bondholders to some chance that their bonds will not be accepted in the tender, and thus they will have to live with a bond modified by the exit consents, which feature so prominently in modern offers.

Introduction

Revlon describes itself “as a color authority and beauty trendsetter in the world of color cosmetics and hair care.”1 Most people would probably just call it a makeup or cosmetics company. For corporate lawyers, Revlon is best known for its classic 1980s hostile takeover, which resulted in the creation of the special “Revlon duties” in Delaware.2 But that hostile takeover and subsequent takeovers of other smaller companies left the company saddled with a tremendous amount of debt, which has burdened the company ever since.3

While it had been struggling with its high debt load for decades, the 2020 COVID-19 pandemic brought a sudden, sharp drop in cosmetic sales.4 And Revlon had $342.8 million of notes (or bonds)5 due in early 2021.6 But it was even worse than that, because under the terms of its loan agreements, if Revlon did not develop a plan to address the maturity of these notes by November 2020, around $1.5 billion of loans would suddenly come due.7 That is, the loans would mature about ninety days before the bonds unless Revlon had the bonds “under control.” As one credit-rating agency explained in summer 2020, “[g]iven the company’s very weak financial performance, Moody’s does not believe that Revlon has sufficient liquidity to repay the notes or that it has the ability to refinance the notes at this time.”8

As a company approaches insolvency—or more vaguely, “financial distress”—American law presents two options for rehabilitation.9 On the one hand, the firm might file for bankruptcy under chapter 11 of the Bankruptcy Code.10 Modern chapter 11 presents a variety of “in court” options for restructuring, ranging from traditional reorganization plans, to prepacks (where the plan is approved by creditors before bankruptcy), to 363 sales (where the debtor sells its assets shortly after filing).11

Alternatively, a distressed company like Revlon might try to come to a deal with its creditors “out of court”—such deals typically being referred to as “workouts.”12 Here, Section 316(b) of the Trust Indenture Act of 1939 (TIA)13 comes into play because it prohibits a majority of bondholders from binding their fellow (dissenting) bondholders to a deal that “impair[s] or affect[s]” the latter’s rights to receive interest or principal when due.14 As one Securities and Exchange Commission (SEC) official said when the TIA was pending before Congress,

If an investor buys a $1,000 bond payable on January 1, 1940, the majority cannot turn it into a $500 bond payable in 1960, without his consent, and without resort to the reorganization machinery now provided by law. There is nothing in this provision, however, which would prevent the majority from waiving its own rights.15

Since direct amendment of a bond contract (known as a bond “indenture”)16 is thus quite arduous—the TIA basically requires unanimous consent17—financially embarrassed corporations most often attempt to effectuate a workout by means of an “exchange offer.”18 As the name implies, this is an offer where the debtor-firm attempts to convince bondholders to exchange their bonds for something new, such as a package of securities and perhaps a bit of cash.19

These offers are loaded with features to make the new package attractive, while making staying in the old bonds as uncomfortable as possible. The latter must be achieved without running afoul of Section 316(b)—that is, our distressed firm will do everything short of “impairing or affecting” bondholders’ rights to receive interest or principal when due.20 In other words, bondholders’ other rights may be impaired or affected without their unanimous consent, just with the consent of a majority of bondholders. And helpfully, from the distressed corporation’s perspective, the courts have read the prohibition on impairing or affecting the right to receive principal and interest when due narrowly, such that debtor-companies can do lots of nasty things to bondholders while still complying with the TIA.21 For example, leaving the company with no assets whatsoever is perfectly fine, so long as the bondholder still has an (ephemeral) contractual right to receive interest and principal from that vacant corporate shell.22

Even if the bond could be amended directly, an exchange offer is often desired from the issuer’s perspective because it allows differing treatment of the assenters (who receive new securities) and the dissenters (who are left behind in the dissipated vestige of their old securities).

Revlon embraced this second approach to tackling its financial problems.23 Specifically, it launched an exchange offer for its $344.8 million of bonds due February 2021, offering for each $1,000 bond tendered either an all-cash option or a combination of cash plus new debt. But the second option was only available to institutional and foreign investors.24

American retail holders were only offered the cash option: $275 in cash, plus a $50 “early tender/consent fee” for those tendering before an early tender deadline. Institutional investors, on the other hand, could either take this cash offer or the other option: $250 cash if tendered by the early deadline,25 plus $145 principal amount of one kind of secured loan, and $217.50 principal amount of another kind of secured loan, for a total of $612.50 for every $1,000 in notes, or .6125 cents on the dollar. Domestic retail bondholders, on the other hand, could at best get .325 cents on the dollar.26

As part of the exchange offer, Revlon solicited bondholder consent to eliminate “substantially all of the restrictive covenants and certain events of default” of the senior notes, and notice that the institutional investors were getting secured debt to replace the old unsecured bonds.27 Retail bondholders were thus faced with the unhappy choice of accepting less return than their fellow bondholders or staying behind in a debt instrument that was stripped of all contractual protections and subordinated in the capital structure. And if these bondholders took too long to think about their options, their return was reduced by $50 per bond.

Despite the aggressive nature of modern exchange offers, the bulk of academic scholarship argues that Section 316(b) should be repealed to allow for yet more innovation in exchange offers.28 In the 1980s, citing the “explosive use of junk bonds” and the growth of institutional investors, Professor Mark Roe promoted repeal of Section 316(b).29 More recently, Professors William Bratton and Adam Levitin, again citing the prevalence of institutional bondholders, have also argued that the prohibition on majority rule is no longer useful and should be repealed.30 Indeed, the ability of institutional investors to “fend for themselves” has been surfaced as an argument against the prohibition, and the TIA more broadly, since even before the Act was passed by Congress.31

As a general matter, this literature argues that bondholders these days are sophisticated investors who can fend for themselves.32 As such, the universe of workouts and exchange offers should be allowed to expand, thus allowing financially distressed companies a more fulsome way to avoid chapter 11, which is conversely seen as an expensive and dreadful fate to be avoided at all costs.

Against this backdrop, I examine the arguments against Section 316(b)—the prohibition on impairment, or the unanimous consent rule, as I sometimes refer to it—of the TIA. At heart, the argument, at least in

the more recent decades, has two parts: first, the prohibition thwarts non-bankruptcy debt restructurings, and second, the prohibition was designed to protect a type of bondholder—the “individual bondholder”—that no longer exists.33 Or stated otherwise, the prohibition or unanimous consent rule is no longer needed, as it is a relic of the New Deal and thwarts useful transactions.

I question both legs of the argument. Namely, I doubt whether the TIA is actually thwarting any useful workouts, and I provide some basic empirical evidence to show that individual bondholders are still quite present in the financial markets. To be sure, the “average” American does not hold individual corporate bonds. But the mythical everywoman (everyman) did not hold individual bonds back in 1939 either.

Today, the standard bond quote from an online brokerage is for twenty-five bonds (or $25,000),34 and since at least the 1890s, corporate bonds have most often traded in minimum increments of $1,000.35 A $1,000 bond trade in 1921 would be the approximate equivalent of a $15,000 trade in 2021.36

Few “average” Americans, today or then, have that kind of money to invest, and even less have that kind of money to invest solely in a single company.37 Referring to such investors as “mom and pop” is more than a bit misleading: they are clearly at least upper middle class, but that does not mean that such investors are unworthy of protection in a clash with Wall Street titans.38

Moreover, through a simple empirical study, we can see that these bondholders are still present in the bond markets. TRACE, FINRA’s over-the-counter price reporting service for the fixed income market, shows frequent trades of $100,000 or less. Institutional investors do not trade in such small increments, and the presence of such trades highlights the exaggerated nature of the casual claim that individuals do not buy bonds “anymore.”39

And while I agree with Bratton and Levitin’s observation that an increasingly large part of the bond market is geared toward investors other than domestic individuals—under Rule 144A40 and Regulation S,41 bonds are frequently sold to institutions and foreigners, respectively—I am reluctant to conclude that individual investors are not present in these markets.42 In support of this point, I provide some data on trading in several distressed bonds below the $100,0000 threshold.43

On the question of exchange offers, and Section 316(b)’s alleged role in reducing the number of useful out-of-court workouts, I note that exchange offers are more common than ever.44 Moreover, they are increasingly brutal in their treatment of retail bondholders, who in modern times are frequently excluded from offers, while the exchange offers subordinate their bonds and strip out every covenant that is not protected by Section 316(b). Why we would want to facilitate even more aggressive workouts, through repeal of the slender protection offered by the unanimous consent rule, is rather unclear.

To make the analysis here more concrete, I examine two recent exchange offers. First, Peabody Energy’s offer, where domestic individual bondholders were excluded from participation, while their bonds were stripped of covenants and subordinated. And I also look at the Revlon 2020 exchange offer, which, as noted, offered public bondholders $250 in cash, while offering institutional investors $612.50 in cash and senior securities. Bondholders who balked at their treatment were again left behind in old bonds that were stripped of covenants, while the consenting institutional bondholders received new senior secured debt.

There is hardly any evidence here to suggest that many exchange offers are being thwarted. Moreover, I question the notion that there is a substantial cost differential between exchange offers and chapter 11.45 While it is easy to see what chapter 11 costs, because all is revealed in open court—and plainly the numbers are substantial—nobody really knows what exchange offers cost.46 The absence of data is too often taken as proof of exchange offer superiority on this front.47

Finally, even if there is a small subset of useful exchange offers that are blocked because of Section 316(b), these can easily be consummated through a prepackaged chapter 11 plan that avoids most of the perceived drawbacks of traditional chapter 11 cases. Indeed, short “24-hour”

prepacks have recently been used in several cases, which calls into question the notion that any meaningful number of truly beneficial restructurings are being thwarted by the Act or Section 316 in particular.48 Indeed, it seems just as likely that the unanimous consent rule mostly thwarts attempts to redistribute value from outsiders to insiders, broadly defined to include those creditors who negotiate the deal with the debtor-firm.

The key sorts of workouts that are barred by the unanimous consent rule are exactly those that no creditor would ever agree to ex ante. Consider, for example, a workout agreement whereby a majority voted to allow the issuer to redeem the bonds for €0.01 per €1,000.49 Why would a majority agree to such a thing? And even if they did so, should that approval be given any respect? Certainly, the bondholder might just be stubborn, holding out for better treatment than they really deserve, but if the group of “holdouts” exceeds more than a trivial amount, it becomes equally plausible that it is the majority vote that is suspect.50 The likelihood of collusion between the issuer-debtor and a majority of friendly bondholders is simply too plausible to ignore in these circumstances.

It is this last point that undergirds the basic conclusion of this Article, that Section 316(b)—the unanimous consent rule—is, if anything, too narrow in its scope. But arguing that the unanimous consent rule is presently too narrow is a far cry from suggesting it should be repealed. Instead, I argue that Section 316(b) should remain as the foundation from which other needed policy reforms can grow. I conclude by arguing that several basic rights that are available to equity holders in tender offers should be extended to debt holders as well, to protect small bondholders from the increasing coercive nature of modern exchange offers.

This Article has four parts. Part I sketches the available tools for restructuring a distressed company and the legal rules that govern each. Namely, such a firm might file a chapter 11 petition or conduct an exchange offer. The latter is governed by the TIA, including Section 316(b), but the debtor-firm can use exit consents, unequal treatment, and threats of subordination to muscle the exchange through.

Part II then reviews the literature surrounding the TIA, and Section 316(b) in particular. Starting with Professor Roe and covering every major article through Bratton and Levitin, this Part traces the more than thirty-year criticism of the unanimous consent rule. The one notable exception is the late Professor Victor Brudney, who argues not only for the retention of Section 316(b), but also an enhanced duty of good faith amongst bondholders and debtors. Professor Brudney suggests that workouts by troubled companies disadvantage individual bondholders and result in inappropriate sharing of gains of avoiding bankruptcy by debtors and bondholders. This Article is very much in sympathy with the Brudney position.

Part III critiques the academic literature, both quantitatively and qualitatively. Starting with the observation that the small individual bondholder was never the “average” American, I demonstrate that the disappearance of such bondholders has been greatly oversold. Next, the question turns to whether the unanimous consent rule prevents useful workouts, and thus forces overly expensive chapter 11 cases. As noted above, I challenge both aspects of this argument: workouts remain plentiful, and the costs of chapter 11 relative to workouts are likely exaggerated. This Part wraps up by noting the aggressive nature of modern exchange offers, and the continuing need for the protections of Section 316(b).

Part IV develops the idea of Section 316(b) as a floor, from which SEC rulemaking can further develop to animate the spirt of the TIA. In particular, by adapting key concepts from equity tender offers—like the “best price” and “all holders” rules—exchange offers can be made more equitable. In addition, I propose a novel two-step technique to address the central problem with exit consents, when bondholders agree to delete terms of bonds moments before they cease to own those bonds.

Because exit consents are currently given by those who will not experience the consequences of their consent, I propose to change that in a way that will result in more considered consent. Namely, through a two-stage process, I expose tendering bondholders to some chance that their bonds will not be accepted in the tender, and thus they will have to live with the bond as modified by the exit consents.

Ultimately, I conclude that the continued existence of Section 316(b), combined with reforms to address the extremes of modern exchange offers, represent sound policy for a world where retail bondholders are still very much in the market.

I. Restructuring Tools

If a large company is worth saving, American law provides two primary mechanisms for restructuring its debt, each of which are outlined below. One obvious method is under chapter 11 of the Bankruptcy Code, a path which itself could involve a variety of sub-techniques that are also noted. Alternatively, the distressed firm might instead attempt to “workout” its problems with creditors. Most often the mechanism that implements the workout will be an exchange offer.

According to data from Moody’s, between 1987 and 2008, about 74% of the total corporate defaults resulted in bankruptcies, while only 16% of defaults were resolved by exchange offers.51 The mix of restructuring tools has substantially changed in recent years: between 2009 and 2017, about half of corporate defaults triggered bankruptcies while more than 40% were addressed by exchange offers.52

According to Moody’s, the factors driving the increased use of exchange offers

include the significant presence of private equity (PE) sponsors as owners of high-yield companies; cost-effectiveness when compared with in-court restructurings that involve many more lawyers and advisers; continued weakening of corporate debt covenants; better overall recovery prospects when compared to bankruptcies; and the incentives for senior bank lenders, who are often in a better position after distressed exchanges are consummated.53

As discussed more fully below, all of these factors—with the possible exception of the cost issue—turn on the ability of an exchange offer to restructure particular classes within the capital structure, while chapter 11 typically sweeps more broadly: traditional chapter 11 cases will address the entire capital structure, and even prepacks (discussed below) will at least cover bond debt and equity.54

According to Standard & Poor’s (S&P), the “average time spent in bankruptcy for companies that exited before 2020 was over eight months.”55 As will be discussed below, exchange offers, particularly exchange offers conducted under the “private placement” exception to the 1933 Act, can be conducted in about a month.

This means that exchange offers can wrap up much quicker than traditional bankruptcy processes, although as also discussed below, prepacked bankruptcy cases are quite similar to exchange offers in terms of duration.56 In addition, S&P has noted that exchange offers may offer something of a pretend solution to financial distress:

Although the appeal of an out-of-court restructuring has increased the number of selective defaults, recidivism is an issue for many of those entities. This raises questions around the efficacy of their out-of-court restructurings.

Based on our data on defaults . . . 208 U.S. and Canadian companies experienced a selective default since 2013. Of these 208 entities, 76 entities (37%) experienced another default either by way of another out-of-court restructuring . . . or a general default or bankruptcy . . . . The odds of these companies experiencing a third default was 22%.57

A. Chapter 11

A chapter 11 case of any form takes place in federal bankruptcy court under the supervision of a bankruptcy judge. While the Bankruptcy Code is heavily focused on “deal making,” the drafters recognized that the traditional corporate law checks on abuse in such deals—shareholder voting and director fiduciary duties—were not apt to operate well in insolvency, where everyone’s incentives and interests are scrambled.58 Thus, while the debtor can conduct “ordinary course” operations without court oversight, non-ordinary activity is subject to judicial review—although typically under a deferential “business judgment” standard.59

Although bankruptcy cases tend to draw upon Delaware corporate law to explain this business judgment standard, it is important to note that bankruptcy arises in a somewhat different context.60 In bankruptcy, the court is engaged in an ex ante evaluation based on whether the debtor’s proposal is substantively reasonable. In Delaware corporate law, the court conducts an ex post evaluation that is based on whether there was adequate process and the merits of the decision are irrelevant. That is, bankruptcy’s business judgment test is substantive, while Delaware’s is procedural.61

As such, it may be that the Delaware case law does not fully translate to the bankruptcy context. But bankruptcy courts and commentators have largely left this point unexplored.62

When drafted in 1978, chapter 11 was primarily designed to foster a negotiation process, after which a reorganization plan would be voted on by creditors and approved (or “confirmed”) by the court.63 But the 1978 Code also included two other provisions that have since provided popular tools when used in conjunction with “normal” chapter 11.

Prepacks have a long, if interrupted, history. Section 77B, enacted in 1934 as the first generally applicable federal corporate reorganization statute, contained a provision for what we would today call a prepackaged reorganization plan: “the plan may be accepted not only before the hearing as to its fairness, but even before the institution of proceedings under Section 77B.”64

The New Dealers did away with “prepacks” for large corporate enterprises in 1938, but they were kept alive in small business cases, and forty years later they came back again with the enactment of the 1978 Code. Section 1125(g) of the Bankruptcy Code provides that “an acceptance or rejection of the plan may be solicited from a holder of a claim or interest if such solicitation complies with applicable nonbankruptcy law and if such holder was solicited before the commencement of the case in a manner complying with applicable nonbankruptcy law.”65

By soliciting votes under non-bankruptcy law, in advance of the case being filed, the time actually spent under the oversight of the bankruptcy judge can be greatly reduced.

In recent years, “24-hour” prepacks have become frequent.66 These one-day cases typically involve restructurings of only the debtor-firm’s syndicated loan.67 More germane for present purposes might be the recent prepackaged case of HighPoint Resources Corporation, which filed a prepack to swap $625 million in unsecured bonds for an equity stake in the reorganized debtor.68 The HighPoint offer was initially structured as an exchange offer, but when the offer did not receive sufficient support, the debtor proceeded with the same basic deal as a prepack.69 The case was filed on March 14, 2021, and the plan was confirmed on March 18, 2021.70 Keeping in mind that there is a solicitation process that happens pre-bankruptcy—covered by the same securities laws that are discussed with regard to exchange offers below71—modern prepacks thus have about the same duration as exchange offers, while offering the ability to bind all creditors to the deal.72

Another way to reduce the disputes that need to be solved within the chapter 11 process is to quickly convert the debtor into a pile of cash.73 In a 363 sale approach to chapter 11—named after Section 363 of the Code, which authorizes such sales—the debtor sells most of its assets in the early days, thus leaving the plan process to dole out the money.74 Complex and contentious questions of valuation—both of the debtor and of any securities given under the plan—are avoided, and the operating assets move through the bankruptcy process with considerable speed.75 The operating company can then proclaim it is “out of bankruptcy,” even if “it” remains in chapter 11 as a matter of corporate law.76

Voting on plans—whether prepackaged or traditional—are subject to the Code’s special two-part voting rule,77 which overrides both contractual terms and the provisions of the TIA.78 As will be noted below, exchange offers often have a high vote threshold—80% or more is quite

common. This is driven by a variety of factors, including the debtor’s need for financial relief, senior lenders who are unwilling to see substantial payments continue to holdout bondholders, and exchanging bondholders who may require high minimum participation conditions to avoid holdouts from remaining in a senior position (e.g., by retaining bonds that mature earlier than the new debt offered in the exchange).79 By offering the same basic deal in the form of a prepack, debtor-firms can bind everyone to the exchange, while only needing to obtain support of more than two-thirds in amount of the bonds.80

Bondholders and other creditors have no direct vote on a 363 sale itself, although they get to vote on the later plan that distributes the sale proceeds.81 At the point of the sale, bondholders’ primary avenue for “voice” is through the hearings to approve the sale process and then the sale itself. Bondholders can object to the sale process and the sale at those hearings, but the sale will be evaluated using the bankruptcy business judgment standard, meaning that it will be approved if it is mostly reasonable.

More generally, and in contrast to the exchange offers discussed below, any of the chapter 11 approaches will happen in federal court. As such, these procedures will involve some degree of transparency, and thus potential unwanted scrutiny for managers and controlling stakeholders. Nevertheless, when evaluating complaints that exchange offers are made too difficult by the TIA, it bears remembering that prepacks and other chapter 11 tools remain as an alternative.

B. Workouts and Exchange Offers

A financially distressed company may attempt to “workout” its problems outside of bankruptcy.82 In theory, this could take the form of a deal to repurchase the outstanding bonds for less than par, but normally a distressed company is short on cash and, in addition, senior credit agreements (“bank loans”) typically limit or prohibit repurchases of junior unsecured debt. As a result, often the only viable option outside of bankruptcy for most distressed bond issuers is an exchange offer.

As the name suggests, an exchange offer is an offer to bondholders to swap existing bonds for something new, with the goal of resolving the debtor’s financial problems.83 Thus, bonds might be exchanged for stock or new debt that matures long in the future.

Exchange offers are used because the TIA, and Section 316(b) in particular, blocks direct amendment of the more relevant terms of the bond.84 That is, the firm in financial distress most often wants to extend the maturity date, reduce the coupon, or even “haircut” bondholders’ principal. As discussed in more detail below, these are the precise changes that Section 316(b) prohibits.

Exchanges of public securities are governed by various regulations under the 1933 Securities Act, the 1934 Exchange Act, and the Trust Indenture Act of 1939.85 Later, this Article will examine the 1934 Act, but here it makes sense to discuss the 1933 Act and the TIA as relevant to exchange offers.

Because exchange offers, particularly in the context of financial distress, typically involve a debtor-firm issuing new securities (in exchange for the old), those securities are potentially subject to the registration requirements of the 1933 Act.86 In a registered debt exchange offer, an issuer must file a registration statement on Form S-4.87 Such an exchange offer cannot proceed until the registration statement is declared effective by the SEC. Due to the delay and cost associated with this process, registered exchange offers are rare, especially in the distressed context.

More common is to proceed under one of two exemptions to the 1933 Act. Section 3(a)(9) of the Securities Act provides a security-based exemption for “any security exchanged by the issuer with its existing security holders exclusively where no commission or other remuneration is paid or given directly or indirectly for soliciting such exchange.”88 If the old bonds were publicly tradable, the new bonds will be as well, a point of contrast with the Section 4(a)(2) offers discussed below.

Notably, this exemption is from the 1933 Act only—any new indenture created as part of the exchange offer will be subject to the qualification requirements of the TIA.89 Note also that a Section 3(a)(9) offer only works when the corporate entity is the same for both the old and new instruments,90 and, as the text of the statute indicates, there are limits on payments that can be made in connection with the exchange.91

If the debtor-issuer prefers not to comply with the obligations of Section 3(a)(9), an exchange offer could be structured as a private offer under Section 4(a)(2).92 Such an issuer needs to determine that a particular bondholder is a sophisticated investor before making an offer to that holder to avoid a “general solicitation” of investors that could make the offer a public offering and subject to registration. That is, under the securities laws, soliciting sophisticated investors—qualified institutional buyers (QIBs) (within the meaning of Rule 144A under the Securities Act) and accredited investors (within the meaning of Regulation D under the Securities Act)93—does not constitute solicitation of the public at large. In addition, in a private placement exchange offer, while the offer of new debt securities is not subject to registration with or review by the SEC, the new securities issued will be “restricted securities” and therefore subject to resale restrictions.

The 1934 Exchange Act instructed the newly formed SEC to conduct a study of corporate restructuring, which until 1933 had been conducted as equity receiverships, largely filed in federal court.94 As a result of that study—overseen by future Supreme Court Justice William O. Douglas—Congress substantially revised the federal corporate bankruptcy laws in 1938, and then enacted the Trust Indenture Act in 1939.95 Under the TIA, bonds, unless the subject of an exemption, must be registered under the 1933 Act and be issued under an indenture that meets the requirements of the TIA and that has been qualified with the SEC.96

Bond indentures have long been negotiated between the issuer-debtor and the underwriters of those bonds.97 As a result, bondholders themselves have little input on the terms, save for the indirect influence larger bondholders might have on underwriters.98 Moreover, most investors, especially retail investors, will rarely see the full indenture before investing in a bond: today, online brokers do not provide them, and the investor has to look for the indenture themselves on the SEC webpage. In prior days, finding the indenture was even more difficult.

It was to address this situation that Congress enacted the TIA. As one leading securities regulation text summarizes:

The Trust Indenture Act of 1939 was enacted to protect “the national public interest and the interest of investors.” The necessity for federal legislation became apparent after years of judicial conflict over the duties of trustees to bondholders and the lack of financial protection afforded even secured bondholders in the chaos that followed the 1929 stock market crash. Exculpatory clauses were included in most indentures and rendered bondholders impotent to hold trustees liable even in those instances in which the trustee’s acts or omissions directly resulted in an injury.99

“In effect, the TIA would be the investor’s silent representative during the drafting of the indenture.”100 As amended in 1990, the TIA perhaps retreats more than a bit from that lofty standard, particularly inasmuch as the statute now permits indenture trustees to operate under conflicts of interest pre-default.101 Of course, indenture trustees were likely never “trustees” in the true sense of the word, despite what the New Dealers may have intended.102 Nonetheless, the statute provides the baseline for all indentures, including those that are not strictly subject to the TIA.103

Most relevant for present purposes, Section 316(b) of the Trust Indenture Act requires that all holders consent to any change in timing or amount of interest and principal payments.104 Section 316(b) was targeted at reorganizations where insiders, or those affiliated with insiders, would agree to amendments that served their other, non-bondholder, interests.105 That is, Section 316(b) is as much about bondholders doing wrong by their fellow bondholders as it is about the debtor-creditor relationship.106

As one commentator observed less than a decade after enactment of the TIA:

[C]ases involving use of majority clauses have disclosed instances where, in securing the vote of security holders, misinformation was supplied or was furnished by biased sources, where votes were cast by those whose interests were adverse to the class being balloted, and where supposedly unbiased fiduciaries participated in the voting and, inadvertently or otherwise, acquired a position adverse to their cestuis, the bondholders.107

The legislative record is replete with comments indicating that Congress hoped to force most restructurings into the daylight through federal bankruptcy proceedings.108 On the other hand, certain comments by then-SEC Commissioner Douglas to the effect that Section 316(b) would not hinder consensual changes to other parts of the indenture allowed the Second Circuit to find that the TIA protected only the specific contractual terms that provide for payment of interest and repayment of principal.109 Changes to any other aspect of the deal, even if it had the practical effect of making such payments improbable, are fair game in federal court—or at least in the Second Circuit.

But the New York Court of Appeals has conversely held that a foreclosure by the trustee, on behalf of a majority of bondholders, did not override the dissenting noteholder’s right to payment or suit. The court based its ruling on the “unanimous consent” provision of the indenture before it, which tracked, as in most indentures, Section 316(b) of the TIA.110

The court noted that while the Second Circuit had dealt with a case where the ability to collect still formally existed—even if it was in practice destroyed—in the case before the New York state courts, the trustee and majority bondholders were arguing that the foreclosure ended bondholders’ ability to collect further.111

There are, of course, countless ways to impair a bondholder’s practical ability to be repaid without eliminating its legal right to repayment, so the New York Court of Appeals decision may be easily evaded in future years, especially if that court is unwilling to go further with its analysis.112

But bondholders can always reject an exchange offer, and if enough reject, the offer will fail. “Because the distressed bonds continue to be valid contracts until surrendered, holdouts can sue for full payment, upending an issuer’s prime motivation for an exchange.”113 For those who are certain that exchange offers are obviously better than chapter 11, holdouts present a serious problem, and indeed much of the academic literature addressed in the following discussion proceeds from that starting point.114 The reasons for bondholder rejection of an exchange offer are many:

Bondholders may believe that the tender price is too low, and therefore wait for a higher price. Creditors may recognize the exchange as merely opportunistic, and therefore, decide to take their chances at normal debt payments, expecting that the company will improve or successfully refinance earlier maturing outstanding debt. However, in today’s environment, a creditor may very well believe that it has better chances of receiving superior value via a bankruptcy or reorganization than it would by accepting the [distressed debt exchange (DDE)]. This is particularly true for certain unsuccessful exchanges when investors likely believe that the proposed DDEs are delaying the inevitable, and that it would be better for the company to file sooner rather than drain value through an exchange that does not alter the [debtor’s cashflow] profile.115

A variety of techniques can be used to inspire participation in the exchange and reduce the number of holdouts. For example, bondholders are often asked to consent to the repeal of all covenants that can be changed by majority rule—typically, this consent is given just before the bondholder swaps into a new security, and as a result, commentators term these “exit consents.”116 Any provision in the indenture that is not the subject of Section 316(b) could potentially be removed by majority vote, leaving the old indenture a shell of its former self.117 Note that the bondholders who consent upon exiting will not face the consequences of their consent.118

Other exchange offers fund an offer for unsecured bonds by means of a secured bank loan or other secured debt.119 As a result, bondholders who refuse to tender will be subordinated in the capital structure. A similar effect can be obtained by providing new debt that is guaranteed

by the operating subsidiaries in a corporate group, when the old debt is a mere obligation of the holding company and thus structurally subordinated.120

Either the exit consents or subordination approach attempt to make remaining in the old debt instrument uncomfortable. And the two are frequently used simultaneously to increase the discomfort.

Modern exchange offers also offer a variety of side payments to induce—or perchance buy—the consent of bondholders.121 Consent fees mean that those who tender quickly get paid more, while the debtor-issuer will often pay the legal and other professional expenses of large bondholders who negotiate the deal as part of an “ad hoc” committee. Likewise, unequal treatment of bondholders, particularly as between institutional and individual holders, is quite possible in this context, even though the securities laws would prohibit the same unequal treatment of shareholders.122

All of these techniques—exit consents, subordination, and side payments—can make an exchange offer coercive.123 As the court noted in Assénagon:

The exit consent is, quite simply, a coercive threat which the issuer invites the majority to levy against the minority, nothing more or less. Its only function is the intimidation of a potential minority, based upon the fear of any individual member of the class that, by rejecting the exchange . . . , he (or it) will be left out in the cold.124

That is, exit consents and other coercive tools can encourage a bondholder to accept an offer that the holder does not believe is optimal, and even to accept an offer that might not be in the interest of bondholders in general.125 A lack of bondholder coordination leaves bondholders guessing about their compatriots’ intentions, and perhaps leads them to accept an offer they would rather reject. A time limited side payment—often tied to early acceptance of the deal—means that the bondholder has to make a quick decision, further limiting the chances for coordination, if she wants to maximize her recovery in the exchange.126

Of course, a bondholder that really wants to hold out can do so. This potentially leaves the debtor company with an annoying “stub” of old debt outstanding, in addition to whatever new securities are issued as part of the exchange offer. Most exchange offers require participation of at least 90% of bondholders.127 And in some cases, the offer is neither attractive enough, nor punitive enough, to get a sufficient mass of bondholders to participate.

On the other hand, even when exchange offers succeed, they often fail to address the firm’s financial distress. The aforementioned 2018 Moody’s study found that between 2010 and 2017, a period of relatively light defaults, ninety-two firms experienced financial distress after having previously addressed financial distress at some point since 1987.128 Of those ninety-two firms, 73% had previously used an exchange offer.

Moreover, in a study of recent energy bankruptcy cases, Moody’s found that the worst outcome for bondholders, measured by recoveries, was to not participate in an exchange offer and then hold on to their bonds all the way through the subsequent (second round) bankruptcy process. Moody’s advises that bondholders are often best served by a “take the money and run” approach to exchange offers, which further encourages acceptance of substandard offers.129

But as will be discussed in Part III, in modern exchange offers, individual bondholders often have no choice but to hold out, as the exchange offer is not even open to them.130 As a result, modern exchange offers will often disproportionately harm retail bondholders.

II. Academic Understandings of Section 316(b)

Professor Roe’s 1987 article, noted in the Introduction, was in the vanguard of a literature that largely developed in the early 1990s, when the bill for the prior decade’s discovery of junk bonds came due.131 Roe’s article starts with the basic points that undergird this literature generally: workouts are less costly than chapter 11, but holding out makes sense in a workout, and the TIA thwarts the obvious solution to the holdout problem, namely restructuring by majority vote.132 Roe also surfaces the major debtor countermoves—namely, subordination of the holdouts and use of exit consents to strip bonds of their covenants—but doubts whether they will really work.133

After reviewing the reasons why the TIA and Section 316(b) were enacted in 1939, Roe then goes on to argue that “the prohibition’s raison d’etre is now gone,” because since 1978, the Bankruptcy Code has only required judges to evaluate a reorganization plan’s fairness in limited contexts.134 Namely, while the New Dealers had wanted to prohibit

private deals in favor of court oversight, court oversight is now greatly reduced, and when combined with the growth of institutional bondholders, Roe concludes that “the voting prohibition is ill-suited to protect bondholders in the 1980’s.”135 Bondholders should instead be protected by a loose standard prohibiting fraud and distortion in bond recapitalizations. Importantly for our later discussion, Roe’s proposal would only allow majority voting in situations without exit consents or side payments.136 This last point was often lost on subsequent commentators—especially practitioners—who embraced repeal of Section 316(b) without engaging with the whole of Roe’s proposal.

While the BLS concluded that the early 1990s recession lasted just eight months—from July 1990 to March 1991—conditions improved quite slowly afterwards, with unemployment nearing 8% as late as June 1992.137 As a result, it is perhaps foreseeable that 1991 saw a windfall of articles on the interplay of exchange offers and the TIA.

Many of these were of the aforementioned practitioner sort, addressing key points of practice as the number of exchange offers ramped up.138 The authors noted the increasing use of exit consents to overcome the problem of Section 316(b)’s prohibition, with one author explaining that “covenant stripping lets the exchange offer proponent do indirectly what it could not do directly: eliminate the control which bondholders may exercise over the company’s financial decision-making and business affairs.”139

In general, the practitioners, as noted above, favored amendment or outright repeal of the section.140 The main academic contributions at this time were a 1991 article by Professors Coffee and Klein,141 and a 1992 article by Professor Brudney which many—including most recently Bratton and Levitin—have interpreted as a rejoinder to Roe.142 Coffee and

Klein built upon a 1990 New York Law Journal article by Professor Coffee, in which he argued that a “combined consent solicitation and tender offer is a technique for maximizing coercive pressure.”143 In the law review article, the authors observe that in an exchange offer, a “bondholder must fear both the issuer’s threats and its fellow bondholders’ opportunism.”144 In particular, they argue that the debtor may proffer an exchange offer to save shareholders, who might be eliminated in a bankruptcy, and the growth of distressed debt investors—which they term “vulture funds”—raises the risk of holdouts within the bondholder class. Thus, it is impossible to know if exit consents and other coercive devices are being used in service of good coercion (to thwart holdouts) or bad coercion (to facilitate equity appropriation).

To overcome this dilemma, the authors argue that exchange offers should proceed in two stages. First, the bondholders should vote on changes to the indenture, and only if those passed should they proceed to decide whether or not to take the offered exchange.145 Bondholders who vote against the “exit consents” could vote to accept the deal consideration in light of their knowledge that the indenture would be amended. Coffee and Klein suggest that either this form of exchange offer, or a prepackaged bankruptcy, should be the only permitted forms for workouts short of full-blown chapter 11 cases.146

They also argue that two Williams Act rules that still today only apply to equity should be expanded to pick up debt tenders offers as well.147 In particular, they argue that Rule 10b-13 (since redesignated as Rule 14e-5)148—which prohibits “side deals” during a pending equity tender offer—should protect bondholders,149 and likewise they argue that consent fees should be prohibited by expansion of the Act’s “best price” rule.150 As the authors explain:

Essentially, a bondholder that votes against the proposed indenture amendment receives a lesser total payment for its bonds than does a bondholder that receives the consent fee. When otherwise identical securities receive different prices in the same tender or exchange offer, the “best price” rule should be seen as violated.151

Professor Brudney then offers the rare defense of the individual bondholder. Specifically, Professor Brudney begins by comparing the plight of bondholders to a hypothetical single lender, noting that bondholders can be encouraged, with “bribes or threats,” to accept a deal that a single lender never would.152 He also notes that, like side payments and exit consents, subordination of old bondholders to those who agree to the exchange “produces a similar effect.”153 And while he concedes that institutional bondholders could band together, he argues their position is still substantially worse than a sole lender, and thus regulation is justified.154

As an initial matter, Professor Brudney urges greater judicial examination of exchange offers: “Difficulties encountered in determining the fairness of a transaction do not justify judicial myopia in examining the coercive or distorting impact on the choices thrust on dispersed debtholders by the strategic behavior of common stockholders.”155

The key aim of such judicial review is consideration of whether the bondholders had given “informed and undistorted” consent.156 He recognizes that Coffee and Klein move in a helpful direction, yet he deems it inadequate, inasmuch as the bondholder is still presented with a take-it-or-leave-it offer.157

Ultimately, he argues that Section 316(b) must be retained, in addition to judicial consideration of the fairness of a transaction.158 While he acknowledges that the TIA facilitates holdouts,

an institutional bias in favor of bondholders is an appropriately heavy weight on the scales which measure whether it is preferable to risk the limited number of bankruptcies that could be avoided by eliminating a hold-out rule than to add a significant uncertainty to the initial cost of all debt by eliminating the buoying-up effect of allowing holdouts.159

In short, Professor Brudney offers one of the few modern defenses of Section 316(b), a point I will circle back to at the conclusion of this Part.

Another relevant entry, often overlooked in this literature, comes from Royce de R. Barondes, then a practitioner but since an academic, who presents an argument that in some sense anticipated the analysis the English High Court utilized in Assénagon.160 Namely, he suggests that agreeing to exit consents in advance of an exchange offer effectively puts the bonds in question under the issuer’s control, since the issuer then knows the bonds will, in all probability, be exchanged as well, and thus the bonds should not “count” for voting purposes.161 Barondes ultimately argues that large bondholders should be publicly identified—as with shareholders under the Williams Act—and the voting patterns of those bondholders in exchange offers should also be disclosed.162

The literature on exchange offers then continued to develop over the next decade, without necessarily directly engaging with the role played by

Section 316(b) of the TIA.163 Nipping on the periphery of this issue, Alan Schwartz suggested that corporations’ inability to waive their right to file bankruptcy was a bigger issue than the TIA,164 while Marcel Kahan, in an article whose title seemed to suggest Section 316(b) would loom large, instead mainly ducked the issue by noting that most indentures include Section 316(b)-style provisions even when they are not subject to the TIA.165 After the turn of the century, there was a further resurgence of interest in the literature, largely driven by a spate of international and sovereign bond restructurings that raised the question of whether Section 316(b), and unanimous consent requirements more generally, should play any important role in those contexts.166

The literature seemed to have run its course as the new century progressed, when two New York district court opinions suddenly reanimated the discourse.167 The opinions in question ruled that aggressive exchange offers could “impair” the rights protected under Section 316(b), even without directly altering those rights themselves. In one case, the issuer paid off one group of bondholders to “stick it” to another. And in the other case, the debtor essentially conducted an old-fashioned equity receivership, where a collusive mortgage foreclosure was used to leave dissenters with claims against an assetless shell. As one district court judge wrote, a quote which was later used by the second judge, it would be “unsatisfying [to hold] that Section 316(b) protects only against formal, explicit modification of the legal right to receive payment, and allows a sufficiently clever issuer to gut the Act’s protections through a transaction such as the one at issue here.”168 The Second Circuit, on the other hand, had no such worries, and restored the TIA to its previous state, holding that Section 316(b) “prohibits only non-consensual amendments to an indenture’s core payment terms.”169

The Second Circuit’s opinion was consistent with a slightly earlier district court opinion, in which the court dismissed a complaint alleging that a debt-for-debt exchange offered only to institutional investors and non-U.S. persons violated Section 316(b).170 According to the court, “Section 316(b) sprang from concerns about majorities abusing minority holders, which did not occur here.”171

This flurry of judicial activity resulted in a corresponding flurry of academic writing on exchange offers and Section 316(b). These new authors again largely adopted the traditional view that “Congress should repeal § 316(b).”172

The most conspicuous example of this second wave literature is the Bratton and Levitin article.173 Noting that exchange offers have become common post-Lehman, the authors also note that “[c]oercive tactics figure more prominently than ever in the new workouts.”174 The authors make three basic claims: first, that exchange offers succeed far more than the first wave of commentators thought; second, that Section 316(b) does not do much in modern finance; and third, that “bond workouts are more coercive than previously thought in some respects, but also less coercive in others.”175 Based on these three points, the authors argue that Section 316(b) should be repealed and replaced with an intra-creditor fiduciary duty, the roots of which they purport to find in the pre-TIA case law.176

Bratton and Levitin argue that exchange offers are more successful now because they are more coercive. They note that more than 80% of all recent exchange offers involve exit consents,177 and more than half involve subordination of old bondholders.178 Many offers also involve selectively made side payments in exchange for tenders—the authors note that about half of exchange offers involve special treatment for consenters, but they also note the widespread use of restructuring support agreements (RSAs) in connection with bankruptcy restructurings.179 Others have noted that RSAs can be a way of offering opaque side benefits to parties that sign on to chapter 11 plans, thus suggesting that side payments are foreseeable in bankruptcy too.180

Bratton and Levitin also suggest that fewer Americans own bonds today than in 1939 when the TIA was enacted, although they only provide post-war data on bond ownership.181 More generally, they note the increasing use of Rule 144A by debt issuers—that is, debt that is never registered for public sale—and argue that exchange offers today are more apt to be conducted under Section 4(a)(2) as private placements (and thus limited to institutional investors) instead of Section 3(a)(9), which provides a general exemption for exchanges with existing bondholders, regardless of their sophistication.182 Moreover, they note the extensive literature on secured creditor control in chapter 11, and thus argue that exchange offers might appeal to unsecured bondholders, given the bondholders’ comparative weakness in modern chapter 11.183 Citing several older studies, they additionally argue that exchange offers also involve lesser direct costs as compared with chapter 11.184

In short, they see a world in which the original aims of Section 316(b)—the protection of individual bondholders—is no longer significant, and in which exchange offers are doing good work. As such, they argue for repeal of Section 316(b), although, as noted, they would couple repeal with adoption of a fiduciary duty to fellow bondholders.185

These claims are evaluated as part of a broader critique of the literature in Part III of this Article.

III. Defending Section 316(b) and the Unanimous Consent Rule

As noted in Part II, much of the scholarship calling for repeal of Section 316(b) rests on the arguments that individual bondholders have left the field, while exchange offers are inherently preferable to chapter 11 cases. That is, bondholders in need of protection are no longer present, so why not make it easier to conduct a helpful exchange offer? In this Part, I question both aspects of this argument.

A. Individual Bondholders

Given the growth of mutual funds and other pooled investments, there is little doubt that the percentage of American corporate bonds owned by individuals directly has declined since the 1929 crash, although there is generally a lack of data covering this entire period.186 We might also worry that the prevalence of individuals invested in high-yield (and thus high-risk) debt is today actually much higher than earlier but obscured by intermediaries like those mutual funds. On the other hand, the bond investor of today, in whatever form, is perhaps more diversified than her counterpart in 1939, inasmuch as a single $1,000 bond today represents less of a commitment to a single debtor-company than the same investment in 1939.187

Individual investors grew as a percentage of the overall population between 1900 and the start of World War I, and during those years some investments were sold on an installment basis to increase participation.188 In the 1920s, there was a general perception that individual investors flooded the market, in part based on individual investors’ experience buying Liberty Bonds during the war.189 Nevertheless, even in the equity markets, where there is better data, there is some suggestion that

individuals who invested directly in the markets were a limited part of the population—just as not all women were flappers in the 1920s, those who speculated in stocks and bonds might have been a narrow but noticeable group of Americans.190

Moreover, in the debt markets, there are indications that the smallest investors were heavily concentrated in foreign bonds, which were heavily marketed to depositors by banks, and real estate debt.191 Both suffered extreme losses after the crash, but neither was the main subject of the Trust Indenture Act, which applies to domestic corporate debt.192 In short, it is unclear how many individuals actually owned corporate bonds in the decade before the crash, and what portion of that group continued to own such bonds well into the Depression.

But if we can draw inferences from the degree of corporate bondholding by financial institutions, it appears that there were not big changes in the market structure between 1920 and 1945.193 For example, financial institutions (mostly banks and life insurance companies) held about 30% of the outstanding corporate bonds in 1920, and that position was largely stable (give or take a few percent) through the end of World War II.194

Immediately after the war, corporate bonds offered returns that paled in comparison with those provided by government savings bonds (for the risk averse individuals) and equities (for the risk seeking).195 As a result, individuals largely left the corporate bond market for other investments, most of which were not options for institutional investors like insurance companies, who thus represented a larger share of the bond market simply by virtue of being the only ones left.

Individual bondholders did not return again until stock prices declined (and interest rates rose) during the late 1960s and into the 1970s.196 Post-war individual bond ownership peaked at just below 20% of the bond market in the mid-1970s, and reached the teens in the mid-1990s and again during the 2008 financial crisis era. As of 2017, institutional investors held about 94% of the corporate bond market, implying that individuals held the remaining 6%.197

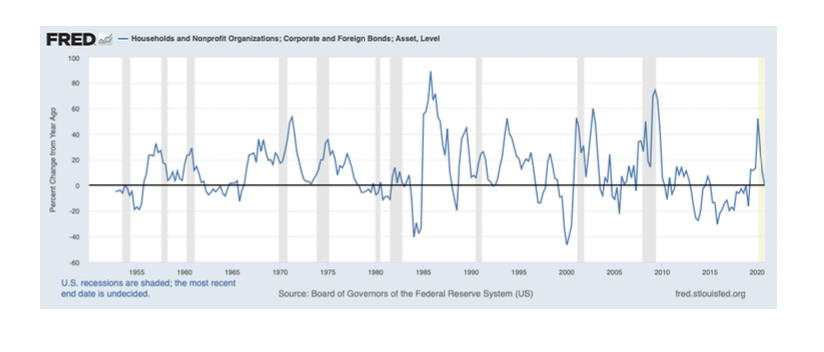

The table below shows the percentage change (from the prior year) of individual corporate bond holdings from 1950.198 As a general matter, the degree of individual debt holding has been quite volatile in the post-war era, tending to rise with declines in the stock market.

But even if individual bondholders only make up about 5% to 10% of the total market today, not only might that change quickly in a coming year—as shown in the graph above—but the dollar values involved are, in any event, still quite substantial, especially given that the U.S. financial

markets are vastly bigger now than they were fifty or one hundred years ago.

Moreover, there are clear signs of individuals, or other small traders, present in the market, perhaps to the same relative degree they were in the late 1930s. For example, in 2014, FINRA reported that there were 10.49 million bond trades of $250,000 or less, which it attributed to “a significant increase in retail participation immediately post-crisis.”199

Current data seems to similarly show the continued presence of retail traders. For example, as of the market close on Friday, April 23, 2021, the second-most traded high-yield bond was an Occidental Petroleum Corporation note due in 2025.200 During the month before (to, and including, March 25), TRACE reported 173 trades in these notes, 105 of which involved a non-dealer customer as counterparty. Of the latter group of trades, 42 trades involved par values of $100,000 or less, and 54 involved trades of $250,000 or less.201 As previously noted, trades below either of these thresholds are apt to reflect retail trading, especially when not amongst dealers.

In short, as much as 31% of the total trades in one month—and more than half of the trades, if we exclude trades between dealers—may have been by retail investors in this “junk” bond. The average (median) trade within the broader retail group was $67,648 ($32,500). And twenty-five trades during this month were for $25,000 or less, thirteen of which were for $10,000 or less—with five for $5,000 or less.202 Trades in these latter groups almost certainly represent retail investors.

Strong evidence of a significant retail presence in one junk bond suggests that the alleged withdrawal of the individual bondholder is overstated. And I find similar results for the month preceding the Peabody and Revlon bonds, which are the subject of the exchange offers examined in Section III.B.

“Peabody Energy, the world’s largest coal company, was producing nearly 20% of all U.S. coal by the time it filed for Chapter 11 protection on April 13, 2016.”203 Despite that earlier and somewhat recent chapter 11 reorganization, it continued to experience financial distress, and on December 24, 2020, it announced an exchange offer involving its 6% senior secured notes due March 2022.204

Peabody’s notes had been issued under Regulation S and Section 4(a)(2), and thus were not formally required to comply with the TIA. Regulation S provides a safe harbor from U.S. registration under the 1933 Act for offshore offers and sales of securities that involve no direct selling efforts in the United States.205 As noted earlier in this Article, Section 4(a)(2) of the Securities Act provides an exemption for “transactions by an issuer not involving any public offering.”206 A “private placement” under Section 4(a)(2) is frequently used in conjunction with Rule 144A of the Securities Act, which provides an exemption for the resale of privately-placed restricted securities only to certain QIBs that are deemed to be sophisticated investors.207 In short, “Rule 144A debt” is privately placed with an initial syndicate of investment banks or “initial purchasers,” who in turn sell these securities to QIB investors. Sometimes Rule 144A debt is later exchanged into TIA qualified debt, with the exemption used simply to bring the bonds to market quickly, but in the case of Peabody, the debt remained unregistered.208

There were eighty-five trades in the Regulation S version of these notes in the month before the exchange offer was made public.209 Thirty-three of these trades involved customers, all but two of which were for $250,000 or less, and indeed the bulk (twenty-nine) were in bonds of $100,000 or less.210 Of the trades for $250,000 or less, the average trade was for $43,903, and the median was $20,000.211

These numbers are especially interesting given that these bonds were (at least in theory) not targeted at domestic retail investors. But it seems entirely probable that debt securities sold under Regulation S could (and in this case did) “flow back” into the United States at some point after they were initially sold to foreign buyers, especially given that the primary resale restriction—Rule 905, under Regulation S—is limited to equity securities. Moreover, if we assume that these notes were “Category 2” securities—debt issued by a reporting United States company212—they would have been subject to at most a forty-day holding period abroad, after which U.S. resales could be conducted under the general exemption in Section 4(a)(1) of the 1933 Act.213

The Rule 144A version of the same notes traded less frequently during the same time period, and in larger amounts.214 There were thirty-nine total trades of this version, eighteen with customers.215 Four of the latter trades were for less than $250,000, but all trades were above $100,000, and thirteen of the customer trades were for more than $1 million.216 Nevertheless, even four trades with a median of $178,000 is somewhat surprising, given that Rule 144A debt is supposed to be limited to institutional investors.217

Similarly, on September 29, 2020, Revlon announced an exchange offer that is also discussed in Section III.B.218 Its 5.75% senior notes due 2021, the subject of the offer, traded 239 times in the preceding month,219 and 104 of these were with customers. Eighty-six of the customer trades were for $100,000 or less, and ninety-two customer trades were for $250,000 or less.220 Of the broader group of potential retail trades (those at $250,000 or less in par value), the average trade was for $40,696, while the median was for $12,500.221

The Revlon notes were TIA-qualified debt, so the lower means and medians and higher trading volumes are to be expected. Nonetheless, an average trade of $40,000, and a median of $12,500, is hardly consistent with the notion that individual bondholders have vanished.222 Indeed, amongst the Revlon trades there are sixty for $25,000 or less—that is, sixty trades in one month that are equal to or less than the default trade in most online brokerage accounts.

In short, retail bondholders are still around. They probably represent a minority of the total bond market, but they may have represented a minority of the total bond market even in the pre-war period. Data on the degree of individual bondholding before the TIA is quite sketchy. Moreover, individual bondholders were never mostly

“moms and pops”—to the extent that term implies either a middle class or “average” American household. The $5,000 trades of the 1940s have become the $25,000 trades of today, but in both cases, the dollar figures were beyond the reach of the average American. The TIA never protected “mom and pop,” nor even George F. Babbitt,223 but rather somebody more like Daisy Buchanan, who has the money to buy individual bonds, but neither the time nor interest to worry about the investment on a day-to-day basis, or to monitor every distressed issuer as it bobs and weaves to avoid a default.224

It is those contortions on the eve of default that we turn to next.

B. The Benefits of Exchange Offers

As noted, the argument against Section 316(b) is comprised of two parts, each of which supports the other. First, as discussed in Section III.A, it is asserted that there are little to no individual bondholders anymore. And second, critics argue that Section 316(b) precludes useful exchange offers. Given the purported lack of individual bondholders, the repeal of Section 316(b), to unleash further exchange offers, is seen as an easy choice.

But are exchange offers actually “better” than chapter 11 reorganizations? The case for an affirmative answer turns on the assertions that exchange offers are cheaper and, perhaps relatedly, that they result in higher returns for creditors.

Pointing in the other direction, Section III.B highlights the uncertain costs of exchange offers, and to note the disparate treatment of small bondholders in modern exchange offers. Moreover, I observe several points that suggest that exchange offers are being used for reasons that have nothing to do with either cost or creditor recoveries, but rather are indicative of the personal benefits insiders see in exchange offers. In short, the concerns that motivated the Trust Indenture Act are still present, and rather than worry that we have too few exchange offers, I worry that we have too many.

1. The Relative Costs of Exchange Offers

The costs of financial distress are routinely split between direct and indirect costs. The direct costs include professional fees associated with tackling distress, while the indirect costs include the less tangible items like managerial distraction and general business underperformance resulting from the distress. The latter costs are presumed to be much larger than the former, but they are also exceedingly difficult to measure.

Moreover, it would seem that indirect costs are apt to be incurred in any state of financial distress, regardless of what mechanism is used to address the situation, and thus they might be of lesser interest from a policy perspective.225 As one commentator noted long ago, “[t]here is a common tendency to view bankruptcy as an ‘either-or’ situation. Either the firm is solvent and there are no costs or the firm is bankrupt and there are costs.”226

There are several recent empirical studies of chapter 11 direct costs which highlight the substantial amount of professional fees incurred in such cases.227 But there is a problem contextualizing these studies, given that most other corporate transactions, including exchange offers, are much less transparent with regard to direct costs.228

Moreover, while chapter 11 costs are usually reported as all of the direct costs incurred while in chapter 11, out-of-court workout costs are typically measured by the costs of the specific procedure. Thus, while

it is easy to think that chapter 11 professional fees are all bankruptcy related, in fact all debtors would . . . incur some amount of professional fees even in the absence of financial distress. . . . [And] if most of the supposed costs of chapter 11 are in fact exogenous to the Bankruptcy Code, . . . changes to chapter 11 will be of slight consequence to the overall ex ante costs of debt finance. Reductions in the cost of chapter 11 may have only a modest correlation with reductions in the cost of financial distress.229

That is, measures of chapter 11 costs likely overstate the “pure” costs of chapter 11 relative to exchange offers, and further, there are few studies of the costs of exchange offers because the costs are often not publicly disclosed.230

The last point does surface the real cost advantage of exchange offers over chapter 11 cases: exchange offers’ relative opacity. Namely, debtor-firm management often resents the transparency of chapter 11, where “a debtor often is said to be ‘operating in a fishbowl’ during the pendency of its chapter 11 case.”231 Exchange offers may offer no direct cost savings whatsoever and management could still find them “cheaper” because exchange offers will not incur the costs associated with transparency.

Of course, the lack of transparency in receiverships is precisely why the New Dealers wanted to force restructurings into open court, where a judge could oversee the fairness of the process. As described in Section III.A, once we reject the notion that individual bondholders are “gone,” one reason for rejecting the New Deal approach to corporate reorganization begins to disappear.

The other reason for rejecting the TIA approach to bonds is that it hinders cheaper, socially beneficial exchange offers. But as just described, nobody really knows how much exchange offers cost, let alone whether they are meaningfully cheaper than something else (most often, chapter 11 cases of some sort). It is conventional wisdom that they are cheaper, but as I have suggested, there could be reasons why management would deem them “cheaper” that have nothing to do with direct or indirect costs. That is, the cost argument could be used as a cover for other factors that are less clearly beneficial to the debtor-firm itself, or society, even while being attractive to managers. In short, the cost argument could be obscuring an agency problem. I return to agency costs below.

2. The True Costs of Modern Exchange Offers

Might exchange offers still be socially beneficial or efficient, even if they are not cheaper than chapter 11 cases? Perhaps, although it is not clear what benefits exchange offers might have that could not be more readily obtained in chapter 11. And recent exchange offer practice should raise concerns that these transactions involve a good deal of appropriation from smaller bondholders.

First, consider the case of Peabody Energy, which, in late December 2020, announced an exchange offer for “any and all of its outstanding 6.000% Senior Secured Notes due 2022.”232 A close reading of the press release makes clear that the offer was not actually for “any and all” of the notes, because it goes on to explain that:

The Offering Memorandum and other documents relating to the Exchange Offer and Consent Solicitation will only be distributed to Eligible Holders of Existing Notes who complete and return an eligibility form confirming that they are either (a) a person that is in the United States and is (i) a “Qualified Institutional Buyer” as that term is defined in Rule 144A under the Securities Act of 1933, as amended (the “Securities Act”), or (ii) an institutional “accredited investor” (within the meaning of Rule 501(a)(1), (2), (3) or (7) under the Securities Act), or (b) a person that is outside the “United States” and is (i) not a “U.S. person,” as those terms are defined in Rule 902 under the Securities Act, and (ii) a “non-U.S. qualified offeree” (as defined in the Offering Memorandum) (such holders, the “Eligible Holders”).233

Since the Offering Memorandum remains hidden, there is no way of knowing the precise definition of some of these terms. But the quoted text certainly suggests that if a retail holder somehow got ahold of some of the notes—and I previously provided some evidence that might have happened, particularly with regard to the Regulation S version—they will not be allowed to participate in the exchange. In essence, they are compelled to become holdouts.

Remaining in the notes had serious consequences for noteholders because it was reported that:

Peabody is soliciting consents to eliminate “substantially all” of the 6% senior secured notes’ restrictive covenants, certain events of default and certain other provisions and to release the collateral securing the notes.234

In short, the senior secured notes became “cov light” notes secured by nothing.235 Along these lines, Peabody reported in January 2021 that:

Approximately 13 percent, or $60.3 million, of the 2022 notes did not participate in the exchange offer, leaving those notes as Peabody’s only funded debt currently maturing prior to December 2024. Given the level of support for the exchange offer, the amendments to the indenture governing the 2022 notes are now operative. As a result, the 2022 notes are now unsecured and will no longer have the benefit of substantially all of the restrictive covenants. The 2022 notes will continue to bear interest at an annual rate of 6.0 percent and mature in March 2022.236

As noted, the debt was not formally subject to the TIA, but it did contain a clause mirroring Section 316(b).237 That thirteen percent of the old bondholders apparently accepted their fate, including being transformed from secured to unsecured debt, provides some further suggestion that small bondholders were very much present in these notes.

Did the exchange offer comport with the contract? As set forth in the margin, the indenture provided an individual right to “receive payment of principal . . . or interest on its Note.”238 The waiver of a lien is at least one step further than exit consents or subordination and seems to go to the core nature of the original obligation between debtor and creditor. The bondholder lent on a secured basis and the borrower has now converted that into an unsecured obligation.

But the indenture is less than clear on this point, with Section 6.07 opening with “[n]otwithstanding any other provision of this Indenture,” but then Section 9.02 allowing for the release of the liens granted under the indenture by a two-thirds vote.239 Most courts would undoubtedly adopt the fiction that an indenture represents a thoughtfully drafted agreement, and decide that the latter provision overrides the former, apart from the unqualified declaration at the outset.240

Regardless of how one comes out on the interpretive issue, we might wonder if there is any social utility in this sort of exchange offer. It seems doubtful that this exchange offer was particularly useful to anyone beyond the debtor and perhaps some distressed debt investor who had bought in at a sufficiently low price relative to par. And if an exchange offer can already strip all covenants from an indenture and render secured debt unsecured, what really is to be gained from repealing Section 316(b) beyond even more extreme restructurings?

Then consider the 2020 Revlon exchange offer for its 5.75% senior notes due 2021, noted in the Introduction and Section III.A, which were subject to the TIA.241 This was actually the second exchange offer Revlon made for these notes: an earlier offer was roundly rejected by bondholders, with only about 5% tendering.242